[This is the second text in the 2024 market overview series. The third and final one, to be published next Saturday, just before Christmas, delivers our own positioning for next year. Don’t miss it!]

Last week we presented the bull 🐂 case for 2024. To summarize quickly, there are three main macro trends driving the bull narrative:

The Fed hiking cycle is finished, disinflation is the clear trend

The economy is strong, resilient, growth is high, recession risk is low

Fiscal policy will be accomodative, the deficit itself carries a stimulus effect

The soft landing narrative is the prevailing bias at this point on markets, no doubt. Especially after this week’s FOMC, where the Fed did a pivot and is now anticipating at least 3 rate cuts next year. A gradual reduction in rates, with the economy remaining resillient is the very definition of a soft landing.

Wall Street analysts, however, have conflicting views on SPX targets for next year. While BofA and Deutsche (among others) project a bullish 5000 target, others like UBS, Goldman, SG, and Wells Fargo are more cautious and see SPX rising only slightly to an average 4,600-4,700. On the bottom of the spectrum is JPMorgan, whose SPX target for next year is 4,200. They represent the biggest bear on the Street for now. As I’ve said last time, these can mean nothing. And most of them were given before this week’s FOMC. In some cases the analyst consensus might even be a decent contrarian indicator. It sure was this time last year.

The bear arguments: hard landing

Today we look at the other side, and present the bear 🐻 case for 2024.

Again let’s start with three main short-term counter-trends that build a contrarian narrative to the bull case:

Growth was high this year, but growth forecasts for 2024 are low, as demand is noticeably slowing, particularly visible in household savings, and bank lending is still in contraction. Even the productivity numbers are not as good as people tend to interpret them. Most major economic indicators are still suggesting a recession is inevitable. A growth contraction will hit earnings, and it will bring equities down. A recession is more likely than is currently priced in.

Wage inflation is still too high, which implies that inflation won’t come down to 2% that easily or quickly. It was one thing bringing inflation down from 9% to 3%, but keeping it sustainably low at 2% when nominal GDP growth is high, is a challenge, especially when asset prices are flying high, bond yields are dropping, and risk appetites are ample (lose financial conditions). The priced-in 125bps of rate cuts (75bps from the Fed) are unrealistic. The Fed could have made a huge mistake this week implying that their job is close to done.

Earnings have, on average, been mediocre, despite high nominal growth. Also, negative earnings surprises in Q3 were punished much more than usual. This is not a bullish sign.

Additionally, there’s a few minor points such as ample geopolitical risks, which could halt the disinflation trend, as well as a number of elections whose outcomes could provide headwinds for economies. But these are mostly “what if” types of scenarios. It’s very difficult to position in the market based on what ifs, unless of course we are tail hedging.

But first, sentiment

There is also a contrarian view on sentiment. If so many are all in for soft landing, there is a very good risk-reward to be positioned on the opposite side, and benefit if/when the majority is proven wrong. If a soft landing is already priced in, it makes sense to bet a little bit on the opposite coming true.

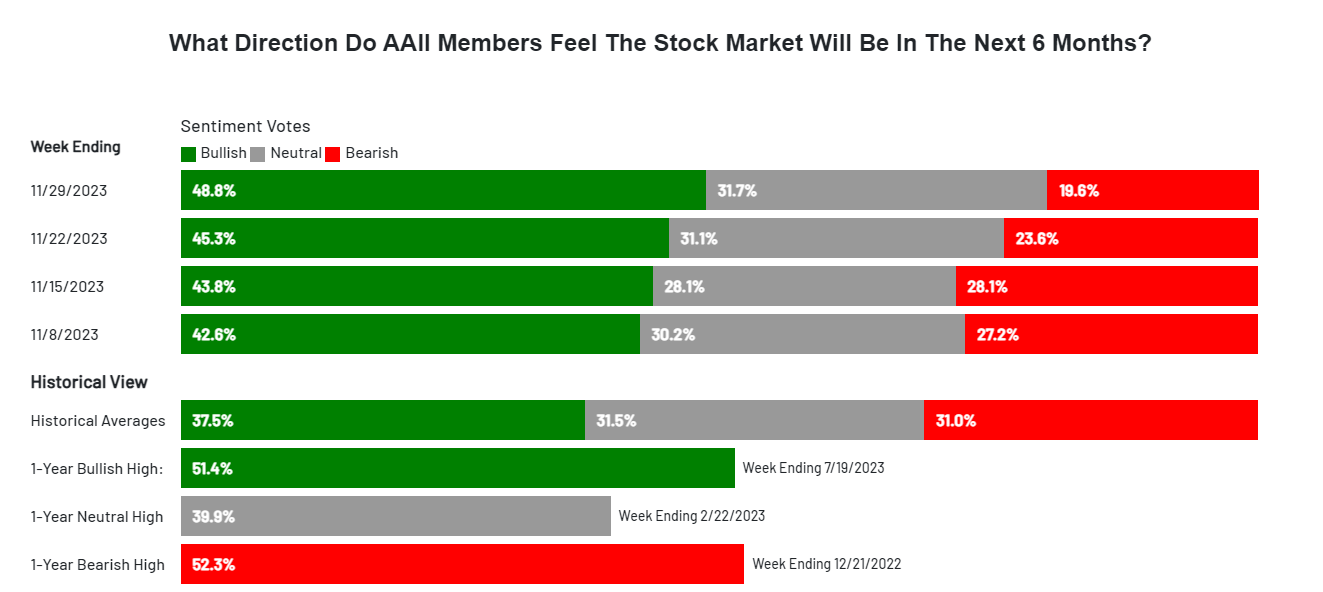

Especially when the Fear&Greed index signals greed (with stock momentum, stock breadth, and the put/call ratio all in extreme greed mode), and even more so if the AAII sentiment survey - often used as a contrarian indicator - signals bullish sentiment over the next 6 months.

Notice where the AAII sentiment was this time last year? Peak bearishness was around Dec 21st last year. What happened in January? The Mag7-driven rally.

Peak bullishness, on the other hand, was on July 19th this year. What happened on July 31st? A three month sell-off. Doesn’t get more contrarian than that!

Current sentiment is basically the inverse of how we entered into 2023. This time last year, investors were predicting a recession (yours truly included), and no one on Wall Street expected a 45% rally in tech stocks after the rout they’ve been through in 2022. This is why so many short squeezes happened. As the majority stayed short, a few early rallies forced them to close these shorts, sending the markets even higher. This was particularly true after the March banking panic. Shorts were deployed, but with markets rebounding, they were reaching their stops and got squeezed out, further amplifying the rally.

Now, with most investors pricing in a soft landing and being long only, the probability of the opposite happening is rising, especially if we get a continued sell-off which will trigger more stops from current positions.

But let’s put sentiment aside for now, and focus on the underlying macro trends and why they might be pushing in the opposite direction of what the bulls believe.