Again with the tariffs?!

After new all-time-highs last week, more uncertainty due to tariffs

Quick summary:

The second week of the Q3 competition is up & running - click here to join the action.

Markets opened Q3 at record highs, with the S&P 500 and Nasdaq finishing last week on strong footing despite light holiday trading.

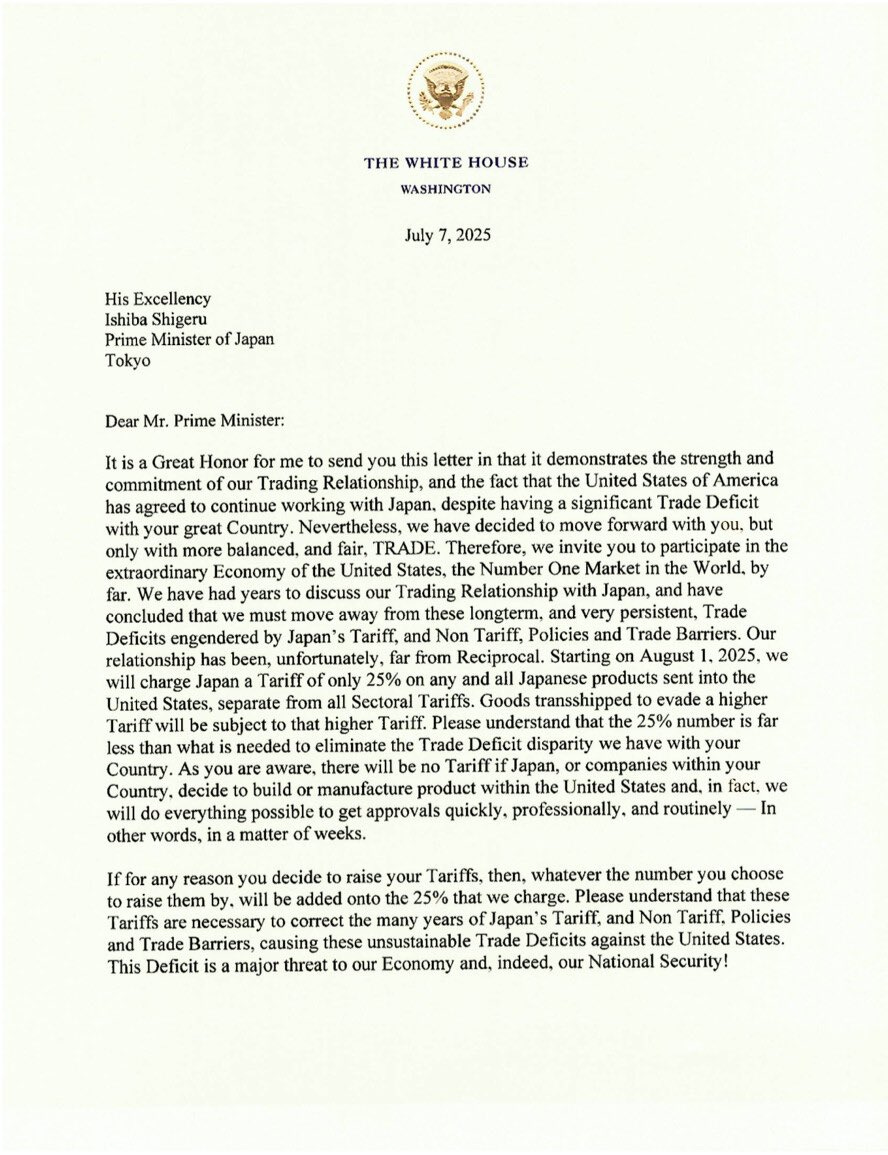

Tariff deadline was extended to August 1st, after the initial 90-day pause ends this week and markets are watching closely to see if the U.S. reinstates elevated import taxes. Trump sent two letters yesterday, to Japan and Korea, telling them they will get a 25% tariffs on all of their products coming into the US. This spooked markets once again.

Fed minutes due Wednesday could clarify how policymakers are viewing inflation and the labor market heading into the next QRA.

Focus remains on policy and the consumer, with macro data like jobless claims and credit levels rounding out the week.

The competition

Markets just closed out record highs, but with tariff uncertainty rising again and Fed minutes hitting Wednesday, this stretch could separate the movers from the drifters. It’s only week 2 of Q3, and there’s still plenty of room to climb!

NOTE: We're sending out all the Q2 prize payments this week. If you haven’t received yours yet, it should show up in your account soon. If not, please do reach out to us.

Keep your strategies sharp and your eyes on the top!

NOTE: For all those new to the whole thing, read more about it here or watch a video of Scott and myself guiding you through the survey, showing you all its features, and briefly explaining how the competition works.

Last week’s performance

Markets are entering Q3 with momentum after finishing June at fresh all-time highs. Last week, both the S&P 500 and Nasdaq closed out with record finishes, supported by a strong Thursday session ahead of the holiday break. While trading was quiet due to the shortened week, all eyes were on Thursday’s June jobs report, which showed the labor market still holding up, though signs of cooling are starting to surface.

The macro backdrop hasn’t shifted much. Core PCE remains elevated at 2.7 percent, and Powell’s stance hasn't changed. Rate cuts remain on hold unless inflation shows more progress. Meanwhile, attention in Washington has zeroed in on Trump’s budget bill and the July 9 tariff deadline, which was extended to August 1st. Markets may move sideways in the short term, but positioning is already starting to reflect anticipation around the next QRA and potential shifts from the Fed.

Then we opened this week with the following double announcement from the President:

One such letter was sent to Japan, the other to South Korea. Same text. Both got the message that they will be getting a 25% tariff on all of their US exports, unless they agree to relocate some of their production to the United States. The deadline for this was extended to August 1st. So in about 3 weeks, Japan and Korea, two very large US trading partners, will get hit by a 25% tariff. There was also a message from Treasury Secretary Bessent that any country which doesn’t make an agreement before Aug 1st will be subject to the April 2nd reciprocal tariffs. Some other countries got their letters as well, with rates over 30%, including Indonesia, Thailand, Cambodia, Serbia, etc.

Equities fell sharply on the news yesterday, while the 10Y shot back up to 4.4%.

The US made some agreements with countries like China and Vietnam (close to a deal with the UK), but there is still no deal with Canada or the EU, so we could very soon regress back to April-level uncertainty.

Also on Wednesday, the Fed will release minutes from its June meeting. This may offer a clearer read on how policymakers are interpreting persistent inflation and labor data. Later in the week, consumer credit levels and initial jobless claims will help round out the macro picture. On the corporate side earnings season hasn’t fully kicked off yet. Delta, Conagra, and Levi Strauss are set to report, but outside the Magnificent Seven, these are more background noise than market drivers. For now, the spotlight stays on policy, the consumer, and what comes next from Washington.

…join the $32,000x competition!

Join our survey competition to get an opportunity to participate in our quarterly ($8000) and annual (3% of our profits) prize distributions:

DISCLAIMER: Neither the survey nor any of the contents of this website can act as investment advice of any kind. The results of the survey need not correspond to actual market preferences or trends, so they should be interpreted with caution. Oraclum Capital, LLC (Henceforth ORCA) is a management company responsible for running the ORCA BASON Fund, LP, and for organizing a survey competition each week, where it invites the subscribers to its newsletter (this website) to participate in an ongoing prediction competition. The information presented on this website and through the survey competition should under no circumstances be used to solicit any investment advice, nor is it allowed to be of commercial use to any of its readers. The survey and this website contain no information that a user may use as financial or investment advice. All rights reserved. Oraclum Capital LLC.

And, as always, don’t forget to subscribe to the newsletter.