Could it be? Higher for longer again!?

Paid subscriber analysis

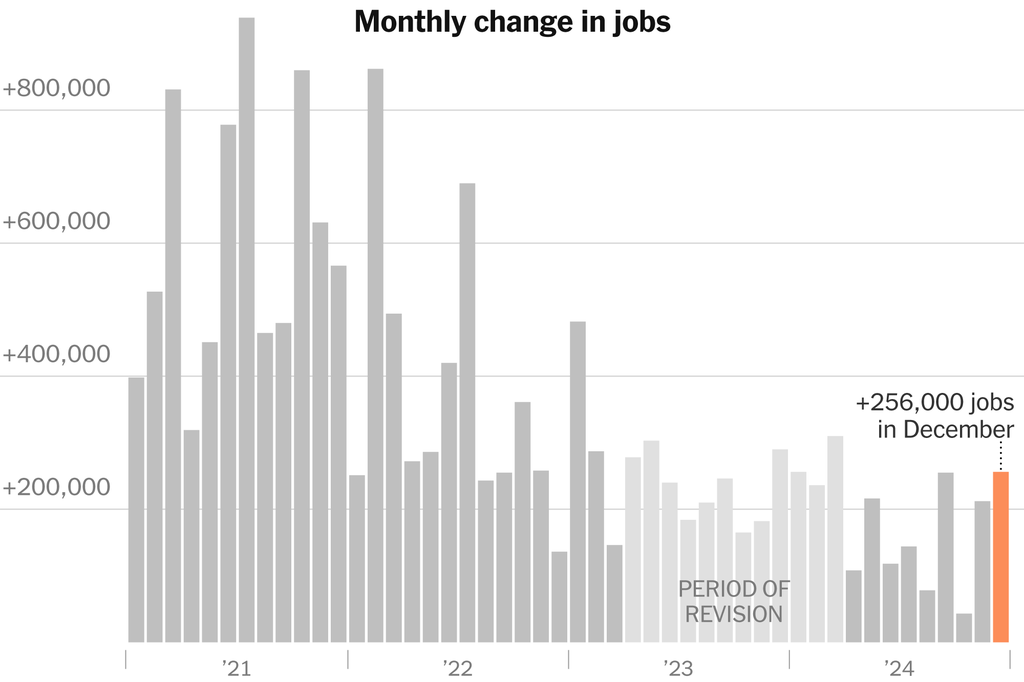

The most recent employment report that came out yesterday showed the US economy created 256,000 new jobs in December, higher than expected, with the unemployment rate going back down to 4.1%. This suggests that the labor market is as strong as ever, with job creation and unemployment both being pretty consistent. The rate hiking cycle that started in 2022 has not put a dent in the US jobs market. We spoke about the structural and cyclical reasons for this many times, but the implication is obvious: no recession in sight.

Oh and yes, GDPNow growth estimate is at 2.7%. No recession indeed.

On the other hand, inflation expectations (Uni of Michigan survey) of US consumers jumped from 3% to 3.3% in the long run, and from 2.8% to 3.3% in the next 12 months. Wage growth is still at 3.9% for last year.

Strong labor market, strong GDP growth, rising inflation expectations - boy, that sure sounds familiar!

No wonder that we got big adjustments in rate cut expectations. The market is now pricing in only a single rate cut in 2025, around the summer. This is more conservative than the Fed estimates from the December FOMC meeting, and a long way from rate cut expectations we have been hearing about for most of last year (expectations of 3% come 2026 - a miss by a total of 100 basis points so far).

The best way to see this divergence between market opinion and FOMC projections are the SOFR forward rates (chart below). Both expect rates to be around 4% before the end of the year, but where FOMC members see them going down to 3% in the next 3 years, the market’s long term view is that rates stay at 4%.

The market is once again becoming anchored at higher for longer.

This doesn’t necessarily make the market right (as nobody really knows if the recession will hit over the next few years), but it is the main reason why the 10-year yield is back at over 4.7%, and climbing higher:

Now this is where it becomes scary.

Last time it was climbing this high it triggered a strong correction in September and October 2023. And then again in April 2024. The first time it was triggered by the Treasury QRA (we covered that in detail many times), and the second time due to (again) higher inflation expectations and anchoring of rate cut expectations (adjusting from 6 down to 3 for 2024).

What does this mean for equities and why? What is an actionable trade from all this?

Subscribe and find out!