Data dependent.

Paid subscriber analysis

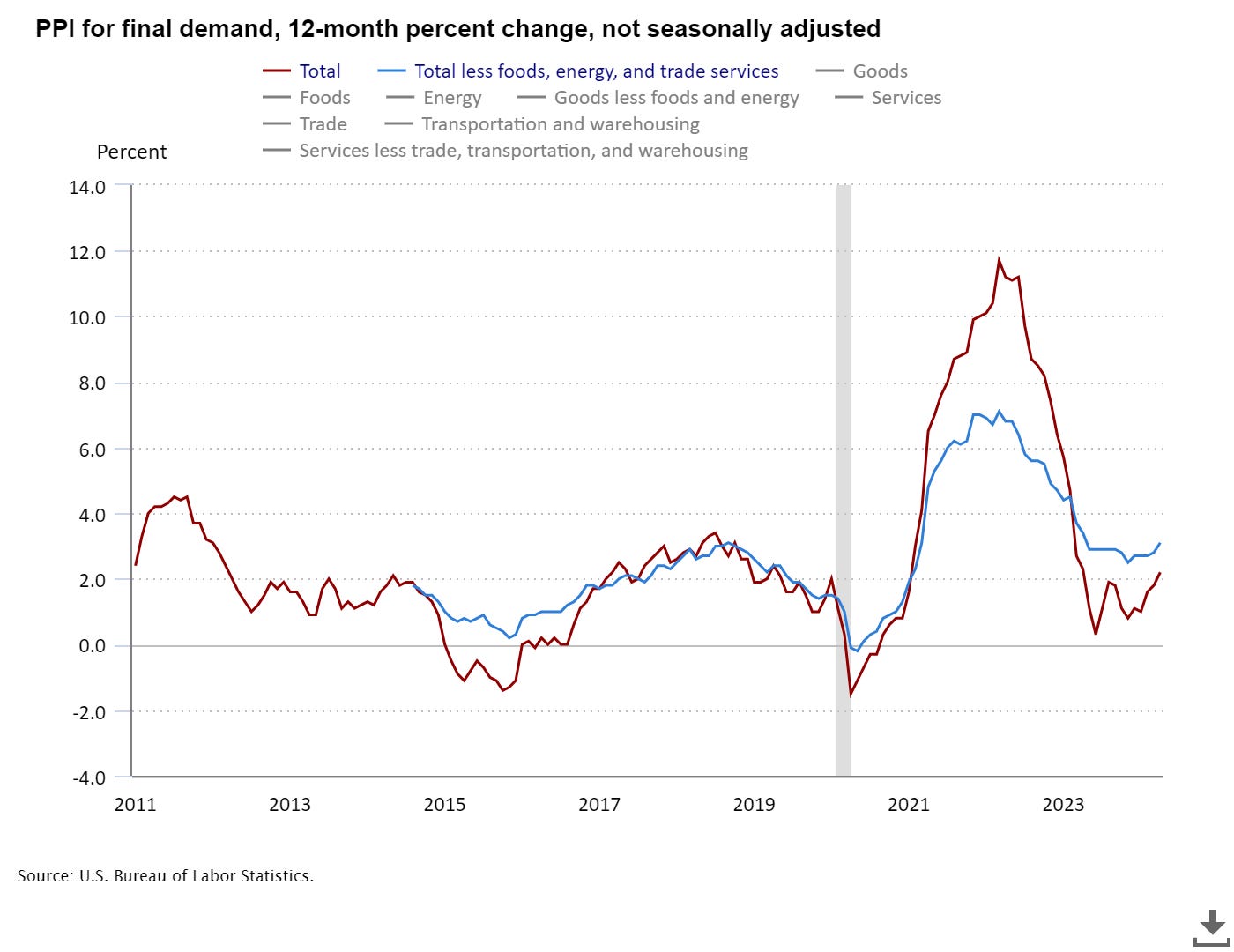

We got the new inflation numbers this week. PPI came in higher (2.2% vs 1.8% in March), but CPI came in lower (3.4% vs 3.5% in March). Core CPI is continuing its downtrend and is now sustainably below 4% (down to 3.6% in April). Core PPI reversed and went up a bit (see figures below). We didn’t get any major change: inflation is still sticky, and housing and transportation are still its main drivers.

However, the market reaction to these numbers was very interesting. On both days, the markets rallied, less on the first, much more on the second day. And rate cut probabilities got repriced again. We’re still at two cuts for this year, but the probabilities are now slightly higher than after FOMC two weeks ago. The market is still very much riding that post-FOMC bullish impulse. We made a correct call coming into FOMC on Apr 27th:

Our baseline scenario for FOMC coming into the week has shifted from bearish to bullish, to which we assign a 67% probability. We expect the deleveraging to have been completed, and that policymakers will be supportive. Had the Thursday sell-off continued into Friday as well (like the week before), the probability of a bullish post-FOMC reaction would have been much higher. The structural flows could do the rest, and we will get a decent buy-the-dip opportunity for the rally into the rest of Q2.

This all happened; deleveraging was done, policymakers supportive (the Fed in particular), structural flows (end/beginning of month + vanna and charm flows) were supportive.

We also expressed caution on May 1st:

“…The Treasury slammed the breaks, but the Fed came to the rescue. So for now, the short term trend should be positive, but in the longer term the headwinds are still there.”

We stand by that assessment. The headwinds are still there, while we are riding the short-term trend up. Powell taking hikes off the table made the key impact back then, despite the volatility. Disturbing this balance will very much depend on the data - if macro conditions start getting progressively worse (slowing growth, rising unemployment, rising inflation), the headwinds will activate. But thus far, that’s not happening.

The significance of this week’s inflation print was in reaffirming the narrative: macro data is still good, inflation is not going up, it’s - at the least - stagnant (sticky), which is known and priced in to the no landing scenario.

Just like Fed, the market is still very much data dependent. And one very important implication here is the positive reaction to bad news on Tuesday. In a bearish environment (e.g. during April), the PPI print would have been punished severely. We got a brief pre-market down reaction, and a rally for the rest of the day. On CPI day - where the news was nothing special - we got a strong rally in all assets: equities, bonds, gold, oil, crypto - the only ones going down were the meme stocks (more on this below). In fact, S&P, NASDAQ and the Dow ended the day on all-time-highs. Dow actually pushed over 40,000 on Thursday (if anything, an important psychological area).