Eyes on the yield curve

And explaining why it matters

This edition of the long Sunday read brings you the most boring topic in finance - bond yields. Yawn. How dull.

But bond yields and the yield curve are actually among the most important things a wary investor should focus on.

So today’s piece will explain the yield curve, why it’s important, why the inverted relationship between bond yields and prices, and why investors keep obsessing about yield curves.

Think of this as piece as the “Everything you wanted to know about bond yields and the yield curve but were too afraid to ask!”

Before we dig in, share to your friends and if you haven’t, feel free to subscribe:

The story of bond yields on US Treasuries ever since the pandemic keeps being a puzzle for the investment community.

First we saw a rise of the 10-year T-bill yield (the reference rate) from 0.53% in July 2020 to 1.1% in January, and then shooting quickly to 1.7% in March (reaching a peak due to inflationary expectation). It then fell back to 1.2% in July, shot up to 1.6% in mid-October and is fluctuating mainly on various inflation reports (this week it shot back up to over 1.5%, a 10% increase, following the high inflation numbers).

What does it mean when bond yields rise? Usually it’s a sign that demand is moving away from T-bills and into other higher-return assets, which is what typically happens during recoveries. It could also be due to higher inflation expectations.

Bond yields and bond prices - a primer

Before moving on, a quick recap of the relationship between bond prices and yields.

Think of it in terms of pure supply and demand. Bond prices and bond yields move inversely. The higher the demand for a bond, the higher its price, and the lower its yield.

Why? Each bond carries a coupon (a payment the bond issuer pays to the buyer/holder of the bond) which remains fixed until maturity. It’s like a loan. You give money to Uncle Sam, they pay you interest every year (or every 6 months) and at the end of the period (say, 10 years), they pay you back the principal.

The yield of a bond is really its current yield, which is the value of the fixed coupon payment divided by the current price of the bond.

For example, a bond is sold for $1000 face value, has a 2% annual coupon rate, meaning that it pays $20 annually to the bearer until maturity. So its initial yield is 20/1000 = 2%.

If there is greater demand for the bond, and its price goes up to, say, $1050, the current yield is 20/1050 = 1.9%.

If the price of the bond goes down due to less demand, say to $920, the current yield jumps to 20/920 = 2.17%.

Hence the inverted relationship between bond yields and bond prices.

So when someone says yields are going up, this means that bond prices are going down – due to a lower demand for bonds (e.g., money going from bonds to stocks). When yields go down, this means bond prices are going up – due to higher demand for bonds (e.g., foreigners buying more US bonds).

Inflation expectations

Which brings us back to the recent yield hikes. Are they really hikes?

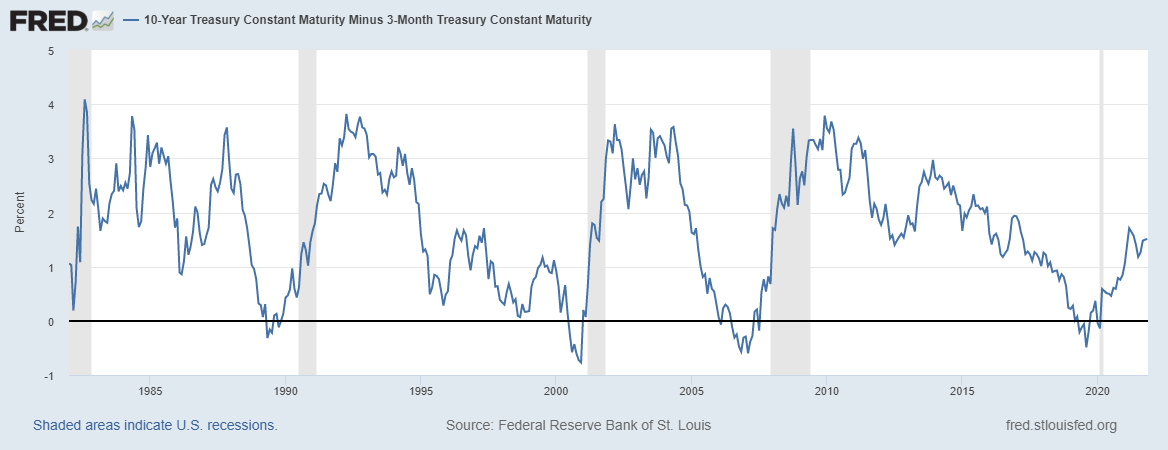

In fact, yields are actually quite low compared to their historical trend. See the chart, the same one from above, but on a much longer time scale, and a clear sign of a secular trend of declining yields. The current rise in yields is hence primarily a signal about short-run investor expectations. A cyclical rather than a structural trend.

Expectations on what exactly?

Inflation.

Bond yields typically go up as a result of several factors:

Demand moving away from Treasuries into higher-return assets, like stocks. This typically happens during times of economic recoveries and/or expansions.

Also, as the US government issued more debt during the pandemic to finance its fiscal packages, so it is increasing the supply of its bonds. Coupled with a slightly weaker demand for Treasuries, it is no surprise that bond prices went down and yields up.

However, in this context, the main reason behind rising bond yields and a steep yield curve are higher inflation expectations. Basically, the market factored in higher inflation expectations already in February and March, and we saw it manifest later in the year (due to many factors, some of which covered here)

How exactly do inflation expectations impact yields? When inflation is expected to be high, you sell bonds, as its low returns are not enough to offset inflation. Lower demand for bonds lowers their price, which increases the yield.

Yield curve explained

Ok, now that this is clear, where does the yield curve come in?

The yield curve shows the relationship between yields and maturities. It shows yields for bonds of the same rating but across different maturities. When someone says yield curve, they typically mean the Treasury yield curve, the benchmark for assessing market debt, and a benchmark for predicting recessions. Typically investors like to observe comparisons between the 3-month, 2-year, 10-year, and 30-year T-bills.

A yield curve can be upward sloping (normal), downward sloping (inverted) or flat.

A normal (steep) yield curve signals an economic expansion and/or higher inflationary expectations. The steeper the curve, the greater the expected expansion (driven by very low short-term interest rates during recovery periods)

A flat curve indicates uncertainty (investors expect similar yields across all maturities during episodes of high uncertainty). It typically occurs at the end of a high growth period (or driven by high inflation expectations), leading to fears of a slowdown.

An inverted yield curve signals an upcoming recession. It is the most important leading indicator of recessions.

Why (and when) does the yield curve invert? Usually, the yield curve is an upwards facing curve, meaning that investors demand greater interest rates for investing in assets with a longer maturity, which makes sense.

You buy a 30-year T-bill and expect to be compensated annually for borrowing your money for such a long period of time (provided that you hold until maturity, which is what most institutional investors do). It's a matter of risk and liquidity premiums; there is greater risk for holding long-term assets.

As the economy starts to overheat, during a period of higher growth and rising inflation expectations, the Fed needs to react and it starts raising short-term interest rates (via the federal funds rate), thus affecting short term Treasury yields (the correlation here is very tight). Yields on short-term rates go up (see yellow curve on the graph above), and stay up as long as the Fed rate is higher.

However, as this continues, and as short-term rates keep going higher, investors become worried about an upcoming recession. Investors then expect that short-term rates will have to fall in the future (because they always do when a crisis is triggered - the Fed will cut rates when the recession happens), so they start buying long-term bonds. Greater demand for long-term bonds increases their price and reduces their yield.

Coupled with the Fed's increase in short-term rates the yield curve begins to flatten and invert.

And so we get an inverted yield curve, where short term interest rates are, counterintuitively, higher than long term rates.

This is a self-perpetuating and reinforcing mechanism that sends signals to investors on how the market is feeling, and at the same time drives reactions of market actors.

When this happens, when the yield curve inverts, which is typically observed by comparing the yield on the 2 year T-bill to the 10 year T-bill (or even better the 3-month yield to the 10-year yield), a crisis happens in the next 6 to 9 months.

Notice when the difference between the 10-year and the 2-year (or 3-month in the second figure) turns negative, a recession is imminent. It’s almost a self-fulfilling prophecy.

What’s happening now?

For one thing, it’s not pointing to a recession.

But there are changes happening in the yield curve.

The figure below shows a comparison between 3 different Treasury yield curves: for May, August, and November 2021. Notice first that all three are still upward slopping. That’s good.

However the November curve (yellow) is starting to flatten a bit – longer maturity yields have clearly gone down since May, while shorter maturity yields are up. Not by much, and not enough to be worried as we still have a very steep upward facing curve indicating a strong economic outlook.

We’re still a long way from an inverted yield curve. That’s the good news.

The bad news is that the Fed is holding the majority of T-bills, even those of longer maturity. This means that it could be sending false signals about the true market value of the yield curve (not allowing demand from market participants to fully determine the price). The Fed always controls short term rates, this is given. But with long-term rates, if the Fed is distorting market signals too much, we might be seeing a slightly distorted version of the yield curve.

However, even if this is the case, the yield curve still would not be inverted, nor close to being inverted. It might just be flatter than what it is now. This is why it will be interesting to watch the yield curve after the Fed starts raising its short term rates (expected by the end of 2022).

Meaning? We’re gonna keep inflating this stock market bubble for most of next year as well. Happy stock picking!

Does the correction in progress change your stance about bubble mention at the end of above article?