Inflation as a prelude into the Fed dot-plot

CPI ahead of the FOMC meeting in two weeks

Quick summary:

The eleventh week of the Q2 competition is up & running - click here to join the action. Three more weeks left in Q2.

SPX closed above 6,000 after the strong May jobs data (139k jobs added, 4.2% unemployment); while bond yields spiked again (10Y at 4.5%, 2Y at 4.0%).

Tesla dropped 15% on Musk vs. Trump drama, but markets quickly moved on.

Wednesday’s CPI report is the main event this week—April inflation was 2.3% YoY; a continued soft print could boost dovish hopes ahead of the June 17–18 Fed meeting.

This weekend, I will review the upcoming FOMC scenarios and probabilities. Don’t miss it.

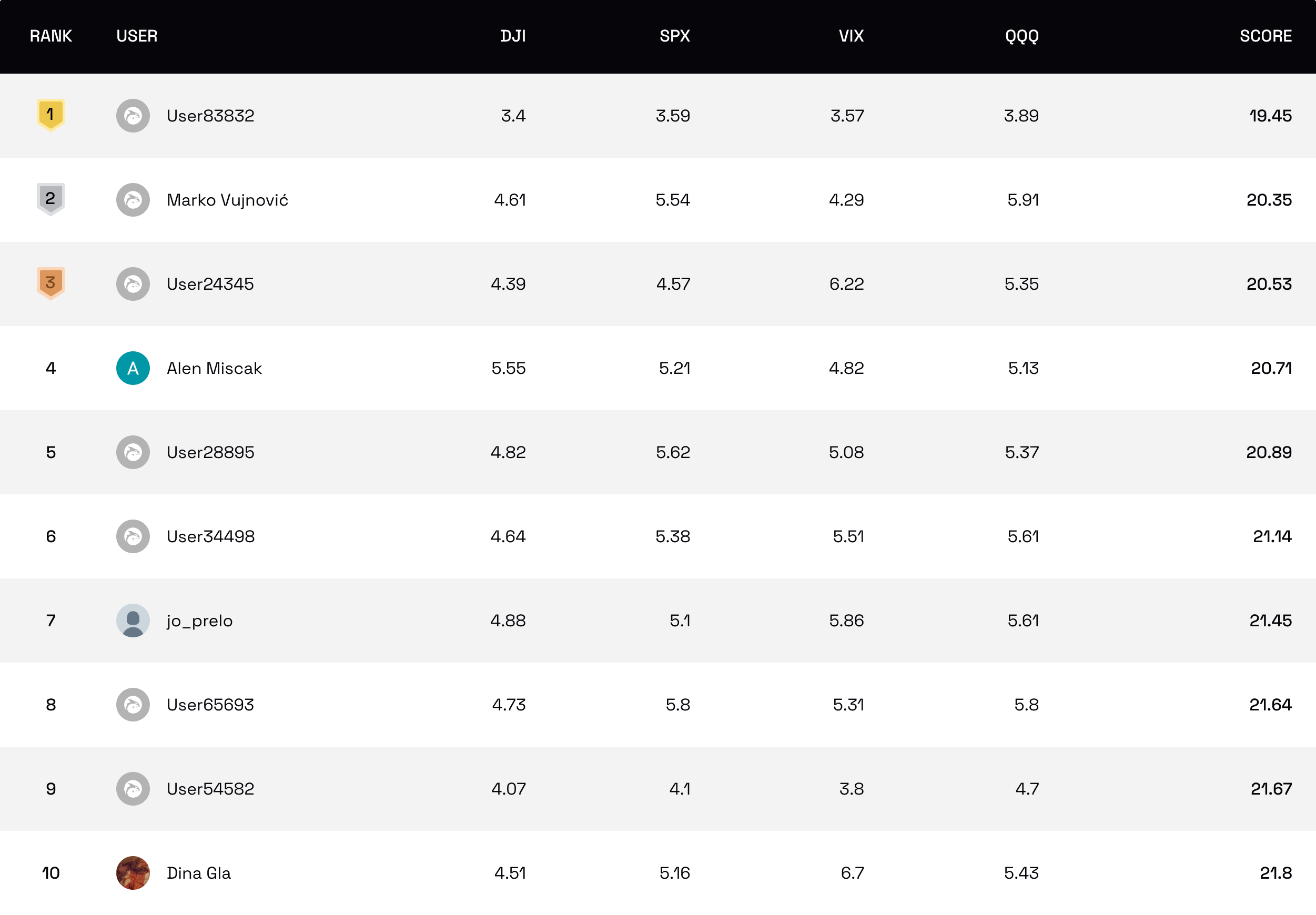

The competition

We’re heading into CPI week with equity momentum building and yields on the move. The leaderboard’s starting to take shape—but with inflation data on deck, one print could flip the script. Let’s see who’s ready to lean into the next move.

Keep your strategies sharp and your eyes on the top!

NOTE: For all those new to the whole thing, read more about it here or watch a video of Scott and myself guiding you through the survey, showing you all its features, and briefly explaining how the competition works.

Last week’s performance

The Musk vs. Trump fallout lit up headlines after Tesla dropped 15% on Thursday, but markets brushed it off by Friday. The real driver was the stronger-than-expected May jobs report—139,000 jobs added, unemployment steady at 4.2%—which helped the S&P 500 reclaim momentum and close just above 6,000, a key technical level. Bond yields followed suit: the 10Y spiked from 4.3% to 4.5% after the report, while the 2Y moved from 3.8% to 4.0%.

Bigger picture, the setup for June is clean. The May-June weakness window? Basically passed. No major sell-off. Inflation data drops next week, FOMC the week after. If the print comes in soft again and the Fed leans dovish—or even hints at a cut—that’s fuel for more upside. Pair that with OpEx and the technical push above 6,000, and we’re staring at the beginning of a low-vol, grind-up summer.

Now all eyes are on Wednesday’s CPI report. April inflation came in at 3.4% year-over-year, and if May shows continued cooling, that could strengthen the case for rate cuts at the Fed’s June 17–18 meeting—something Trump has been openly pushing. A softer CPI would likely ease bond yields and support further upside in equities. If inflation continues to comes in light, risk assets may catch another leg higher. But a hot CPI print could flip that script fast.

…join the $32,000x competition!

Join our survey competition to get an opportunity to participate in our quarterly ($8000) and annual (3% of our profits) prize distributions:

DISCLAIMER: Neither the survey nor any of the contents of this website can act as investment advice of any kind. The results of the survey need not correspond to actual market preferences or trends, so they should be interpreted with caution. Oraclum Capital, LLC (Henceforth ORCA) is a management company responsible for running the ORCA BASON Fund, LP, and for organizing a survey competition each week, where it invites the subscribers to its newsletter (this website) to participate in an ongoing prediction competition. The information presented on this website and through the survey competition should under no circumstances be used to solicit any investment advice, nor is it allowed to be of commercial use to any of its readers. The survey and this website contain no information that a user may use as financial or investment advice. All rights reserved. Oraclum Capital LLC.

And, as always, don’t forget to subscribe to the newsletter.