Is inflation peaking: redux

The war is likely to reverse the easing of supply chain pressures

The new CPI report came out this week, showing that inflation is still at a 30-year high, up by 7.9% for the 12-month period (0.8% monthly increase).

In my previous analysis I suggested that inflation is likely to start going down soon given the easing of supply chain pressures worldwide. Several indicators were showing peak supply chain pressure in October and November 2021, suggesting that inflation was, in fact, peaking in Q1 2022.

But then the war in Ukraine started.

And we’re back to square one.

The new CPI number didn’t even take into account the escalation in prices due to the war in Ukraine and Russian sanctions (it was February data, while prices really started hiking in the first week of March).

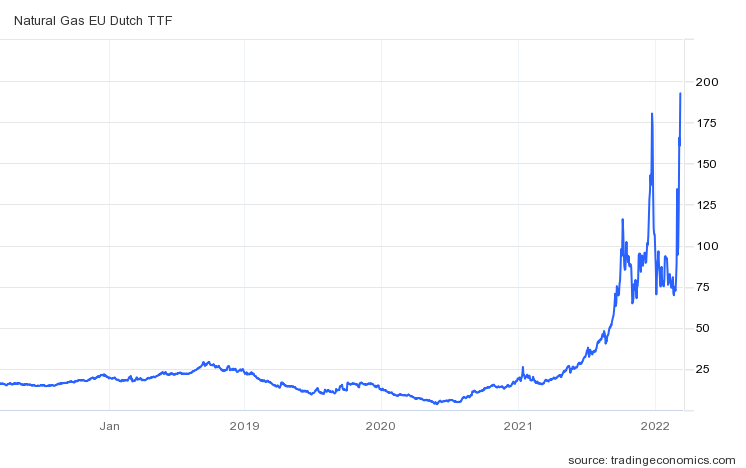

Oil, gas, and some food and commodity prices all started peaking again, even higher than their Q4 2021 levels (below are charts for wheat and European natural gas).

Oil went up from $92 to $125 in two weeks (35% increase).

Why? A huge chunk of oil supply has been pulled off the market. Firms are not buying Russian oil out of fear of negative repercussions (e.g. being accused of financing the war). Russian oil producers started offering oil at 25% discount but are still struggling to find buyers (Shell, however, did take advantage of the discount, even though they apologized a few days later and said they won’t do it again).

The same happened to all major food and commodity items being produced in Russia and Ukraine. Exports have stopped or have been significantly reduced. Global supply is down, and prices, amidst high demand, are up.

So instead of easing the supply chain (as many indicators have suggested), domestic demand will once again be faced with replacing suppliers (just like during COVID). This is costly, takes time, and puts additional strains on the supply chain as new suppliers become overwhelmed with higher demand.

It’s happening again!

Higher inflation will, unfortunately, be an inevitable outcome.

Recession worries?

Oil is up so much (and it might continue to go up) that many investors are now even more concerned of a recession.

Oil prices have often been used as a predictive indicator of recessions, even though it’s most likely a mere correlation. In other words, the same pressures pushing up oil are driving the business cycle to its peak, forcing the Fed to react and initiate the cycle’s late-stage recessionary spiral.

How exactly does this work?

Oil prices are an important contributor to CPI. They are a key source of today’s high inflation as well. It’s easy to see why. Huge demand for oil across the economy (businesses and consumers) affects everyone’s budget. This was particularly a problem during the stagflationary 1970s (which is why many are evoking that decade today).

When oil goes up, it adds to inflationary pressures, and expectations of rate increases go up. Other things are happening as well, so the Fed might have to raise rates anyway, but high oil prices certainly amplify the need for the Fed to do so. And when the Fed starts raising rates, we enter the late stages of the business cycle.

What’s that?

Lower interest rates are applied during recessions to kick-start the recovery (cheap borrowing spurs demand). They are kept low until the economy starts to "overheat" (a typical sign was higher inflation). As the economy overheats, the Fed raises rates to prevent inflation.

High rates affect mortgages, borrowing costs, disposable income, consumption, and soon enough corporate earnings. With demand going down, layoffs are inevitable, and the reinforcing negative spiral continues.

This time, however, while oil prices are booming, expectations of a rate hike in March are strongly anchored around only a 25bps increase. In fact, the dreaded 50bps increase is completely off the table for next week’s Fed meeting (the graph below used to show probabilities for a 25bps hike along a 50bps hike, but it now assigns 0% probability to a 50bps hike, and even a 4% probability that rates stay as they are).

So why aren’t investors pricing in higher rate hikes?

They actually are, over a more medium term. The graphs below show higher expectations for the 10-year inflation rate, and the 5-year forward inflation expectation rate. Notice that both have spiked since the war started, and were easing just before that.

The war changed the narrative. The Fed won’t slam on the breaks too hard, because they're afraid that economic consequences of the war might increase recessionary pressures.

The Fed was in a very difficult position before the war was even announced. Their decision is still balancing on tightrope. Should they:

hike strongly in the near term to increase credibility vis-a-vis inflation, but by doing so increase the probability of recession?

Orhike less strongly, lose credibility over inflation, but prevent recession in the near term?

There are no best-case scenarios any more. If the supply chain easing had continued this would have reduced some pressure off the Fed. But then the war started, and it'll bring us back to November's highs.

We are up for a hard landing or a crash, a soft landing is no longer a viable outcome.

So yeah, we can blame it on Putin then 😄 (the meme will be right! - last part at least)

What should an investor do?

If you haven’t already, now is probably a good time to re-balance your portfolio. Sell and/or reduce some of your riskier exposures (like cyclicals or tech except the big 4), and go long commodities. ETFs are the most convenient way of doing this.

You can go long oil via USO, long gold via GLD, and long food and commodities via DBC or PDBC. Also, increase your cash holdings for now (long on the US dollar).

These are short-term plays that should be good risk hedges until the war in Ukraine is resolved, or when price pressures subside (this should coincide with the end of the war).

Also, watch the Fed and bond yields for sings of yield curve inversions (TBT is a good instrument here - a post on this is coming up soon). And remember, always keep a nice little SPY tail-hedge.

DISCLAIMER: This blog post does not act as financial or investment advice of any kind. Oraclum bears no responsibility for your personal investment choices, as they always depend on each individual’s different risk profiles and existing exposure.

broad inflation exposure is available via RLY ETF. crash hedge via TAIL. or everything together, simpler, via all-weather RPAR