Peak disinflation sentiment?

Paid subscriber analysis

Very interesting reactions to the CPI on Thursday and PPI on Friday. Almost exactly the opposite of expectations in both cases.

Let’s do Thursday first.

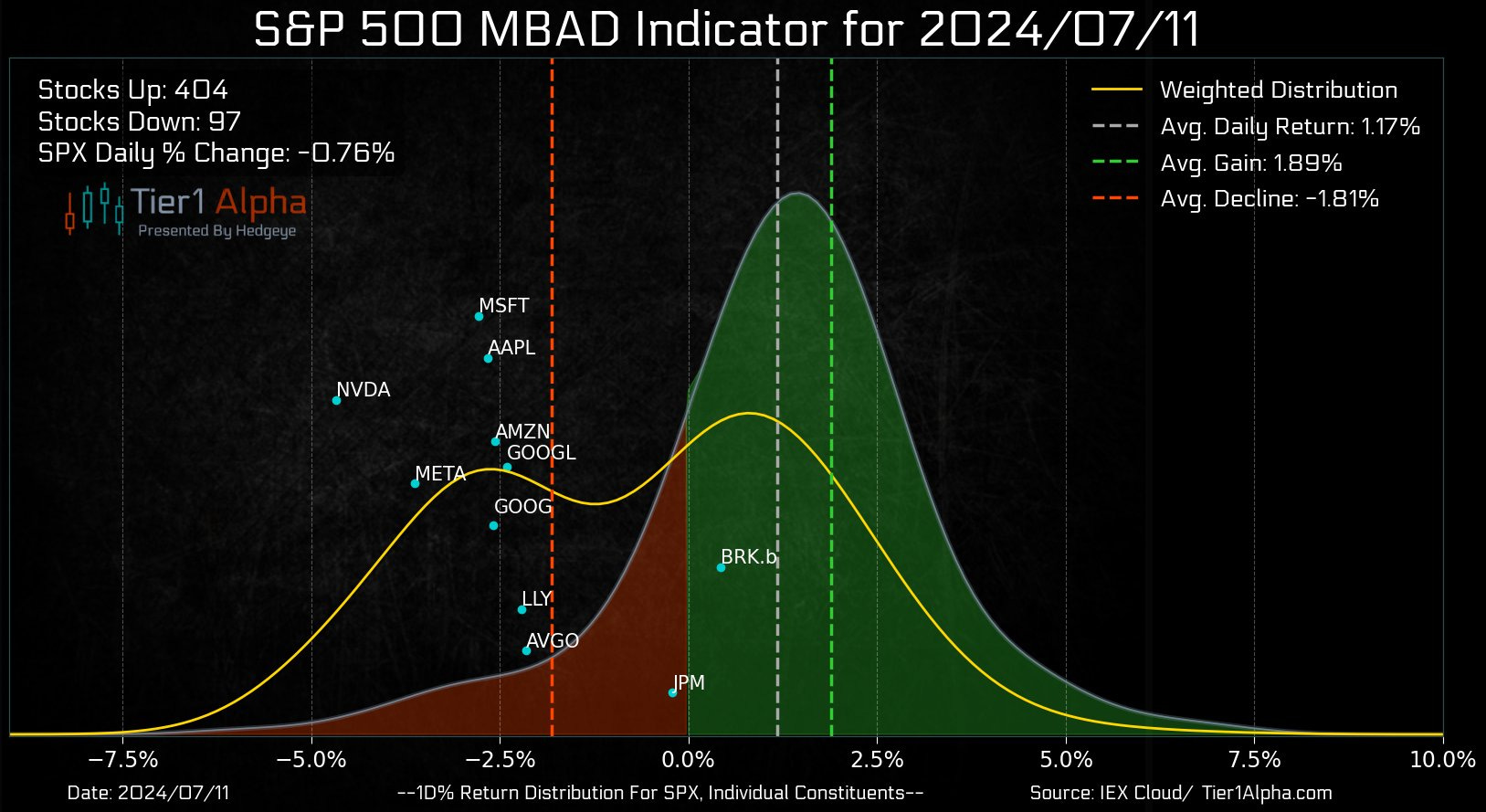

After a better than expected CPI report (-0.1% m-o-m, and down to 3% annually) we got a rally in bonds, a super strong rally in small caps (IWM ended the day +3.5%), and, surprisingly, a sell-off in equities, driven primarily by the Mag7.

80% of the SPX was up on Thursday, but the sell-off was driven by a handful of the very same stocks that keep driving this market up for the past two years:

CPI inflation came in at 3% and the trend down is clear, whether we look at the 1-month, 3-month or 6-month averages:

Rate cut expectations surged almost immediately - there is now a 90% probability of a cut in September.

But beneath the surface, if you look at the composition, the sell-off of Mag7 made sense. These were the sector returns from Thursday:

Notice the rotation: from tech (the bottom three sectors are all dominated by the Mag7 - with AMZN and TSLA being in the Consumer discretionary category) to small caps in real estate, utilities, materials, industrials - estimated to benefit the most from a rate cut. In other words taking some profits from Mag7 and spreading them across the aisle.

And then on Friday, the exact opposite reaction. A worse than expected PPI report (trending up instead of down, was 2.6% annually versus 2.3% expected), but the markets pull off a complete reversal (at least until the final 30 minutes). Equities (SPX, NDQ, or should I say Mag7) up, small caps and bonds continued up as well, although less than the day before.

Clearly other things were the drivers of yet another jumpy week. Friday’s option flows (vanna and charm) were strong enough to keep the momentum (also as the pull down factor into the close yesterday), but obviously we got some idea of what the sentiment might feel like from now on.

Specifically, if we are entering a period of disinflation, which means pricing in Fed cuts more aggressively (no point in staying at 5.5% if inflation is on a steady path to 2%), can we expect a rate cut because we are pricing in a soft landing, or because we are expecting a slowdown?

In other words, has the positive disinflation narrative reached its peak, meaning that, from now on, further declines in inflation are actually projecting a slowdown in economic activity?

Let’s review how this new information fits into our three scenarios.

Recall what we wrote on June 15th:

Three scenarios:

No Landing - high growth, robust labor markets, sticky inflation => higher rates, no need to cut. Sideways-up markets.

Trading strategy: Equities buy and hold, no excess trading as swings are likely. Short bonds, as yields likely to keep creeping up (especially due to Treasury issuance).

Slowdown/recession - GDP starts to lag, labor markets begin to show weakness (unemployment going up to 4.2% or more, less jobs creation), inflation might be going down due to the slowdown of economic activity => there will be cuts, but not as a sign of good news. Equities likely to be hurt as earnings start to go bad.

Trading strategy: short bias for equities (meaning keep a larger hedge to benefit from sell-offs). Long bonds (due to rate cuts and recession signals)

Soft Landing: high growth, robust labor markets, but decreasing inflation => lower interest rates for all the good reasons. Strong rally in markets.

Trading strategy: Long equities, long bonds.