Rangebound or breakout?

PCE report this Friday, vol still going down

Quick summary:

It’s our last week for the Q1 competition! - click here to join the action. Good luck to all of you fighting for the top spots!

NOTE: This is the final week where daylight savings times are different for US and EU participants. Juts a note that it’s an hour earlier, still.

Last week, the Fed kept rates unchanged and maintained its 2025 economic outlook, while lowering GDP growth to 1.7% and raising core inflation expectations to 2.8%.

Markets saw mild relief as volatility dropped, but SPX remained range-bound between 5,600 and 5,700.

This week’s focus is on Friday’s PCE inflation data on Friday, along with consumer sentiment and housing market reports.

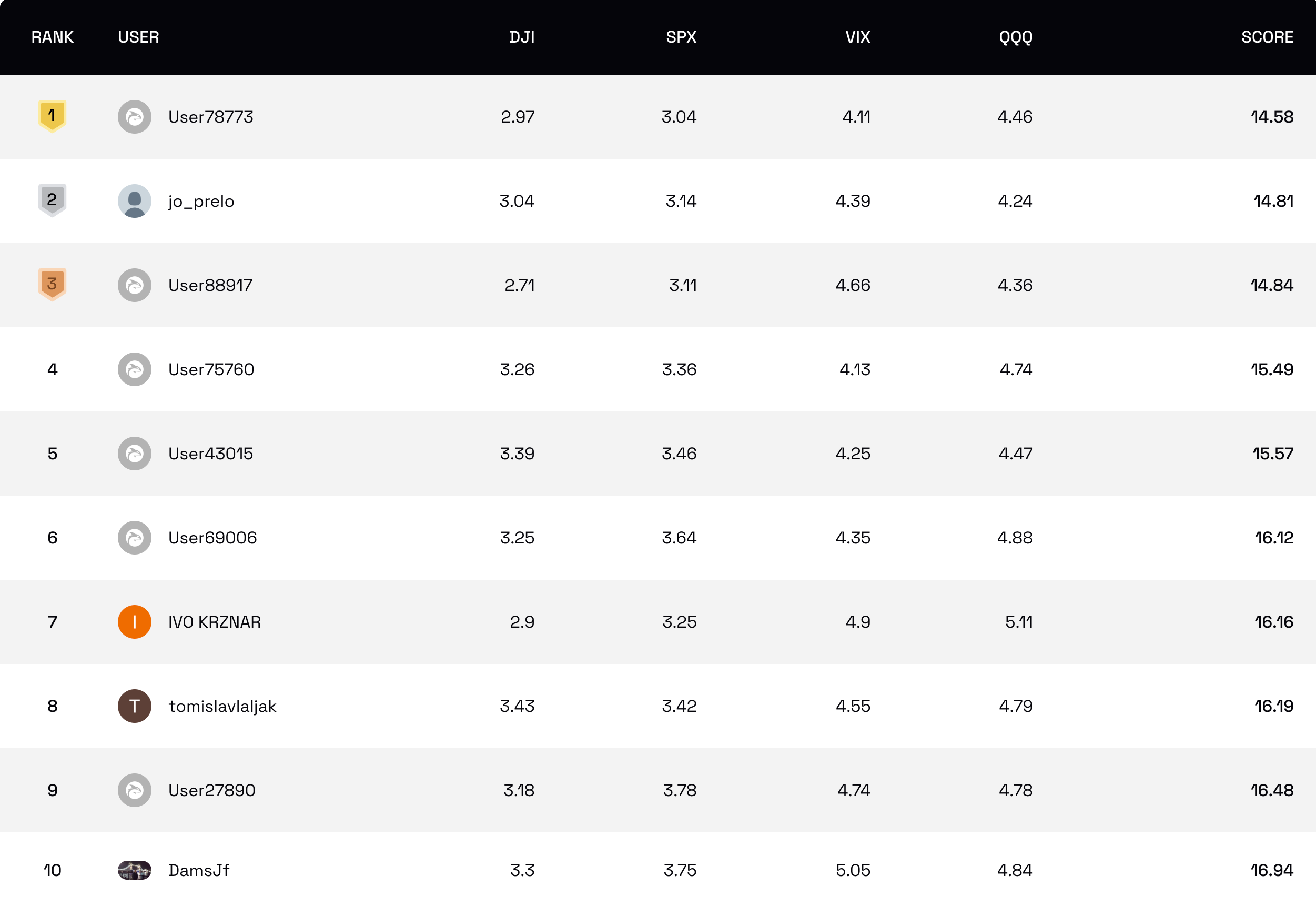

The competition

It’s the last week of Q1, and the leaderboard’s close—every small edge matters from here on out. Good luck to all of you fighting for the top spots this quarter. The margins up top are still razor thin!

Don’t forget about the survey open and close at 8am ET and that this is an hour earlier than usual due to DST.

Keep your strategies sharp and your eyes on the top!

NOTE: For all those new to the whole thing, read more about it here or watch a video of Scott and myself guiding you through the survey, showing you all its features, and briefly explaining how the competition works.

Last week’s performance

Fed delivered a predictable update: no shifts in interest rates and steady projections for 2025, holding at two anticipated rate cuts and a stable long-term rate of 3%. Notably, GDP growth expectations for 2025 were lowered from 2.1% to 1.7%, and inflation forecasts were nudged up, with core inflation expected to hit 2.8%. In a bullish turn, the Fed announced a slowdown in quantitative tightening, easing the monthly redemption cap on Treasury securities significantly starting in April.

Market response? A dip in volatility. The VIX fell below 20, sparking a mild relief rally, though the S&P 500 struggled, repeatedly testing but not surpassing the 5,700 level. It hovered mostly between 5,600 and 5,700, suggesting a tentative market not quite ready to commit to a stronger rally.

Looking forward, the stage is set for a cautious buildup to the earnings season. The current market dynamics hint at a potential setup for another downturn, mirroring patterns seen in previous years. As we edge into this critical period, keeping an eye on upcoming earnings in April will be key to understanding the next major market moves.

As for this week, markets will focus on the release of the PCE index due Friday, which will provide updated insights into inflation pressures. This is particularly significant after January's data suggested a cooling trend, despite the Fed's adjustments to its economic projections.

We were trading rangebound last week, between 5,600 and 5,700. Perhaps this week the range shifts to a higher level. Or we get a nice breakout until April earnings. Let’s see.

…join the $32,000x competition!

Join our survey competition to get an opportunity to participate in our quarterly ($8000) and annual (3% of our profits) prize distributions:

DISCLAIMER: Neither the survey nor any of the contents of this website can act as investment advice of any kind. The results of the survey need not correspond to actual market preferences or trends, so they should be interpreted with caution. Oraclum Capital, LLC (Henceforth ORCA) is a management company responsible for running the ORCA BASON Fund, LP, and for organizing a survey competition each week, where it invites the subscribers to its newsletter (this website) to participate in an ongoing prediction competition. The information presented on this website and through the survey competition should under no circumstances be used to solicit any investment advice, nor is it allowed to be of commercial use to any of its readers. The survey and this website contain no information that a user may use as financial or investment advice. All rights reserved. Oraclum Capital LLC.

And, as always, don’t forget to subscribe to the newsletter.