Sell in May, and go away?

With May OPEX behind us, here's how might markets shape up

There’s a trader mantra for almost every situation you can find in markets. Very often there’s more than one for each scenario, so that you can find an adequate ex post justification for whatever happened. My favorite is “Don’t fight the Fed”, which can also mean whatever you want. For example, in the current environment the bears might say: “rates are high, this will crush the economy, #DontFightTheFed, the market is going down”, whereas the bulls might say: “hikes are pausing, the Fed is signaling a soft landing, #DontFightTheFed, the market is going up”.

So today, let’s take on another famous mantra: “sell in May, and go away”.

Short term logic

Yesterday’s monthly options expiry (OPEX) for May kicked in. Markets rallied strongly during the week (we made a decent prediction and return, but that’s for Tuesday’s post), the shorts have been squeezed, and volume was higher. Last time we had a similar environment was after February OPEX, Feb 17. The market decline started the day after Feb OPEX and lasted until the March OPEX, Mar 17, pushing SPX down by over 160 points (see figure below). Some of it was, obviously, due to the banking panic in the second week of March (as was the subsequent bounce-back the week later), but notice that February too finished about 120 points lower after OPEX. Ever since March 17th, we had a melt-up in equities, gradually squeezing the shorts and pushing SPX above 4200 for the first time since August (similar for NASDAQ, also going above its August ‘22 high).

What is OPEX and why it matters in this case?

Many traders like to use the options market as a signaling mechanism of how the equity market might react. By definition, option prices react to equity prices: when a stock price goes up, you make money buying call options (lose if selling calls), which tend to significantly appreciate in value. When a stock price goes down, you make money buying put options (lose if selling puts). However, many traders have figured out that the options tail often gets to wag the equities dog, where huge flows into calls or puts at times of strong rallies or sell-offs tends to amplify those rallies or sell-offs with option dealers hedging bets from traders by taking the opposite side of that bet, as they need to remain delta neutral. I highly recommend this YT channel if you wanna familiarize yourself more with this.

Ok, but what do the May or February OPEX have to do with this? Well, there is typically large open interest for options at quarterly expiry (Mar, Jun, Sep, Dec) - this would be institutionals changing their positioning, typically with large moves that tend to move markets significantly. It doesn’t happen at every OPEX month prior to quarterly expiry, but when there are many factors pointing to the direction of a potential pullback (like they were back in February), then it makes sense to pay attention and take some risk off in equity positioning.

What other factors are at play? The most important one, the Fed, is still adamant in their higher for longer approach (as Powell mentioned yesterday), keeping interest rates at over 5% this year, despite the markets expecting otherwise over the next few months. It has now been 15 months since the Fed started raising rates, which is typically a time lag for what it takes demand in the economy to slow down and reflect these changes. Economic numbers (jobs, housing, retail sales) are suggesting the beginning of a gradual decline.

Then the there is the issue of the US debt ceiling cliffhanger (we’ve gone through quite a few of these over the years). The danger is that the President and Congress do not reach a deal before the June 1st deadline, meaning that the US might default on its debt. The chances of this happening are almost negligent (so there is no real danger from the debt ceiling becoming a catalyst for a brutal market sell-off), but the implications of the deal being reached are also interesting. An increase in the debt ceiling means the Treasury is going to take on new debt to finance government operations, meaning that it will issue a whole new batch of T-Bills onto the market. A fresh supply of bonds would decrease their price, pushing yields up, but also putting more downward pressure on the equity market. Another short-term headwind for equities that adds well to the “sell in May” narrative.

Long term logic

What about the long term?

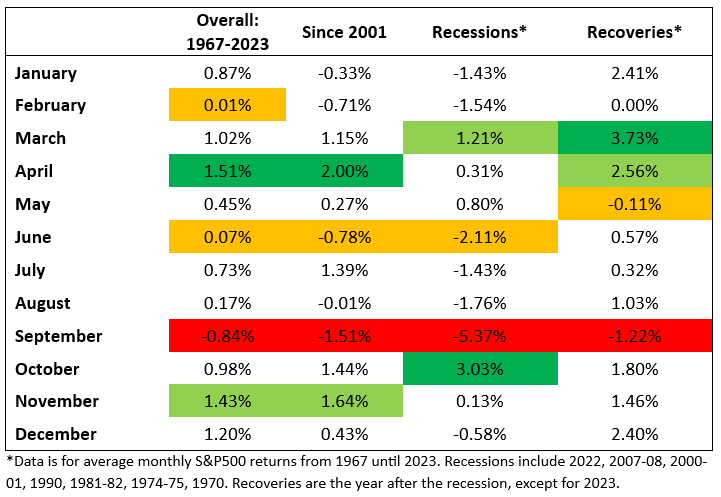

The table below looks at the average monthly S&P500 returns over the past 56 years, from 1967 to 2023. It’s split into four columns; monthly returns overall, over the past 20 years, during recessions, and during recoveries (definitions given below the table). The worst performing month of each period is labelled red and the second (or third) worst are labelled orange. The best performing month for each period is labelled dark green, and the second best light green.

A few interesting trends. September tends to be the worst performing month, often by a wide margin, across every period. June is very often the second worst performer, closely followed by August, February, and May. So purely based on this data, selling in May, which tends to be a subpar performer overall, and not going back in until after September seems to be a quite decent strategy in the long run. Visually we get the same inference:

With one caveat. Sell in May, but make sure to buy back in October as the final quarter of the year tends to be very good for equities, even during recessions (with October typically being the short covering month following September’s decline). The best performing month across the 56-year sample, however, is April, with March and November following closely behind.

The long term trends therefore seem to confirm the “sell in May” mantra (obviously exceptions are always possible), and this year, so do the short term implications. For any long positions, we would argue that now is the right time to put some hedges.

Let’s see how it plays out.

We’re back with our regular update on Tuesday, have a great weekend!

DISCLAIMER: None of the contents of this website can act as investment advice of any kind. Oraclum Capital, LLC (Henceforth ORCA) is a management company responsible for running the ORCA BASON Fund, LP, and for organizing a survey competition each week, where it invites the subscribers to its newsletter (this website) to participate in an ongoing prediction competition. The information presented on this website should under no circumstances be used to solicit any investment advice, nor is it allowed to be of commercial use to any of its readers. This website contains no information that a user may use as financial or investment advice. All rights reserved. Oraclum Capital LLC.

And, as always, don’t forget to share & subscribe!