The view from all time highs.

Paid subscriber analysis

This turned out to be a fun week. SPX joined the NDX (NASDAQ 100) in reaching an all time high. Driven by the tech rally over Thursday and Friday, SPX pierced through 4,800 and consolidated, after having failed to do so on several occasions the past few weeks. Purely on technical terms, this is a bullish sign.

However, notice what also shot up this week. Bond yields!

NDX was up 2.8% and SPX 1.2% (they started the week selling off), but the 10Y went up by 4.6%, and the 2Y went up by 5.6%. The 10Y yield is now once again above 4.1%, and the 2Y is above 4.3%. We are therefore ending the week with both equities and yields up (bonds down).

The bond market move was a clear reaction to all the economic data we had this week. Labor markets are still robust (hot even), as is the economy in general, and coupled with a stickier than expected inflation, there is certainly less room for the Fed to starting cutting rates sooner. At least this is what was priced in for the week.

We are basically back to the #2 macro scenario from our playbook: yields going up, despite inflation on a much lower level, waiting for a catalyst, and still no sign of weakness for the economy. Furthermore, the 2Y10Y and the 3M10Y both remain inverted (obviously, as short duration bonds are still aligned with the Fed funds rate).

It’s like this whole week has been a repeat of 2023! Tech-driven equity rallies, the economy is strong, bond yields are going up alongside equities, and bears are falling victim to short squeezes (as did the BASON this week, but more on that on Tuesday).

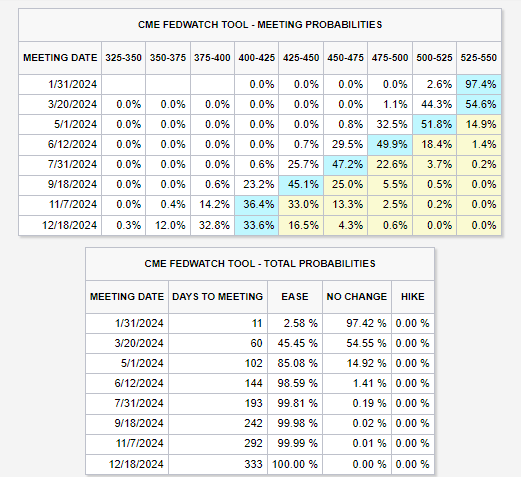

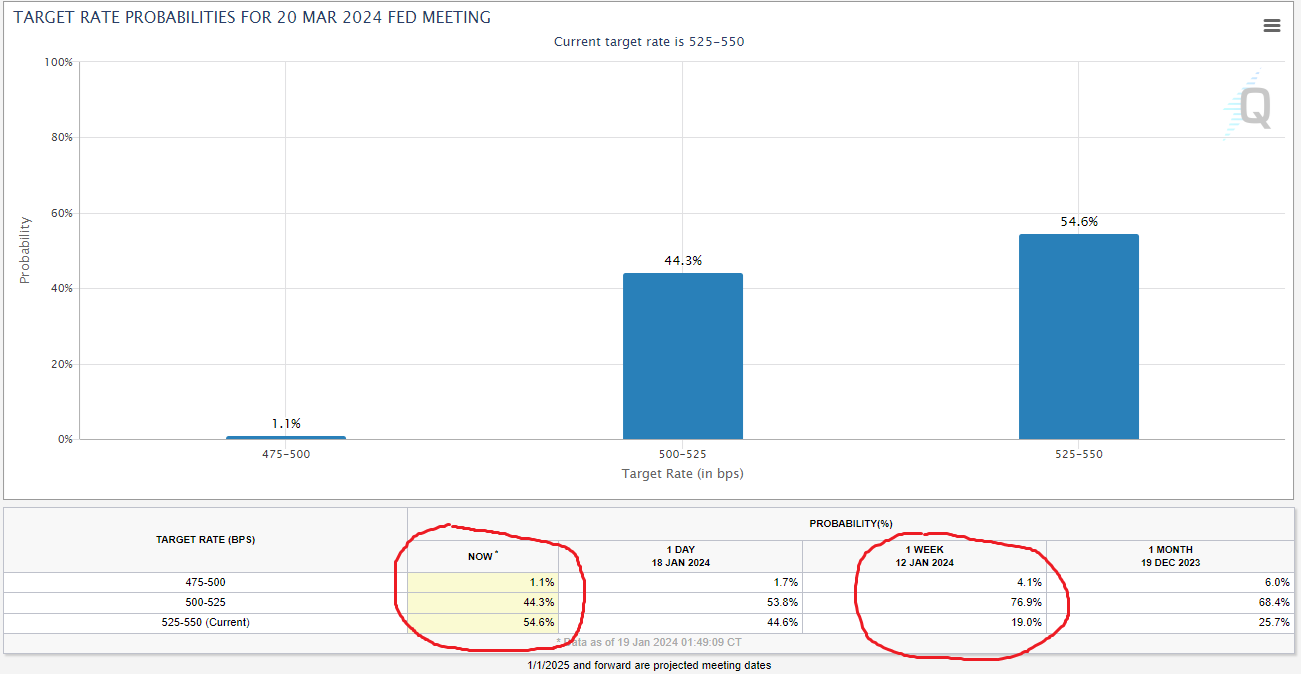

However, have a look at this interesting development, the update in FOMC rate cut probabilities, amidst a week when equities made all-time highs. The March meeting probabilities are now marginally in favor of another pause, rather than a cut. Markets are now pricing in 5 cuts instead of 6 this year.

A week ago, the chances of a rate cut in March were 77%. As of yesterday, after a week of good economic data, they have fallen down to 44%. Why is that?

Again, economic data from this week. Most leading indicators suggested an economy that is doing quite well. It this economic environment, and with core inflation still sticky, investors start thinking that the Fed might not have to cut just yet.

But shouldn’t this be bad for equities? Why did they reach an all time high then?