What to do with SpaceX?

Premium analysis - free for all

This is an example of a Premium subscription article, which we have introduced as a new part of the newsletter, accompanying our incredible Dashboard. Premium articles will all be free until August 1st.

Summary:

On Friday we get the biggest IPO in history: SpaceX is open for trading (ticker is SPCX) when the market opens. Expect a few minutes of price discovery and high volatility after 9:30 before it starts to go. Options trading will start on Monday.

SpaceX is an internet provider wearing an AI costume. Starlink is 61% of revenue and the only profitable segment. The $28.5tn total addressable market (TAM) estimate is 93% AI - including $22.7tn of “enterprise applications” that’s bigger than every economy except the US and China. The number isn’t a target, it’s wishful thinking.

Three businesses, three clocks, one price tag. Starlink drives the cash today, Starship is the hinge next (no orbital payload yet, $3bn per year to feed it), and AI is the lottery ticket for someday (xAI burns $10bn per year). You’re paying the 2028 price in 2026. Not ideal for a value investor.

The only disinterested number says it’s worth half of what they claim. Morningstar pegs fair value at $780bn against the $1.77tn offer - roughly 94x sales. Everyone else quoted in this deal gets paid if it pops. Again, pure growth stock, looking to ride on momentum.

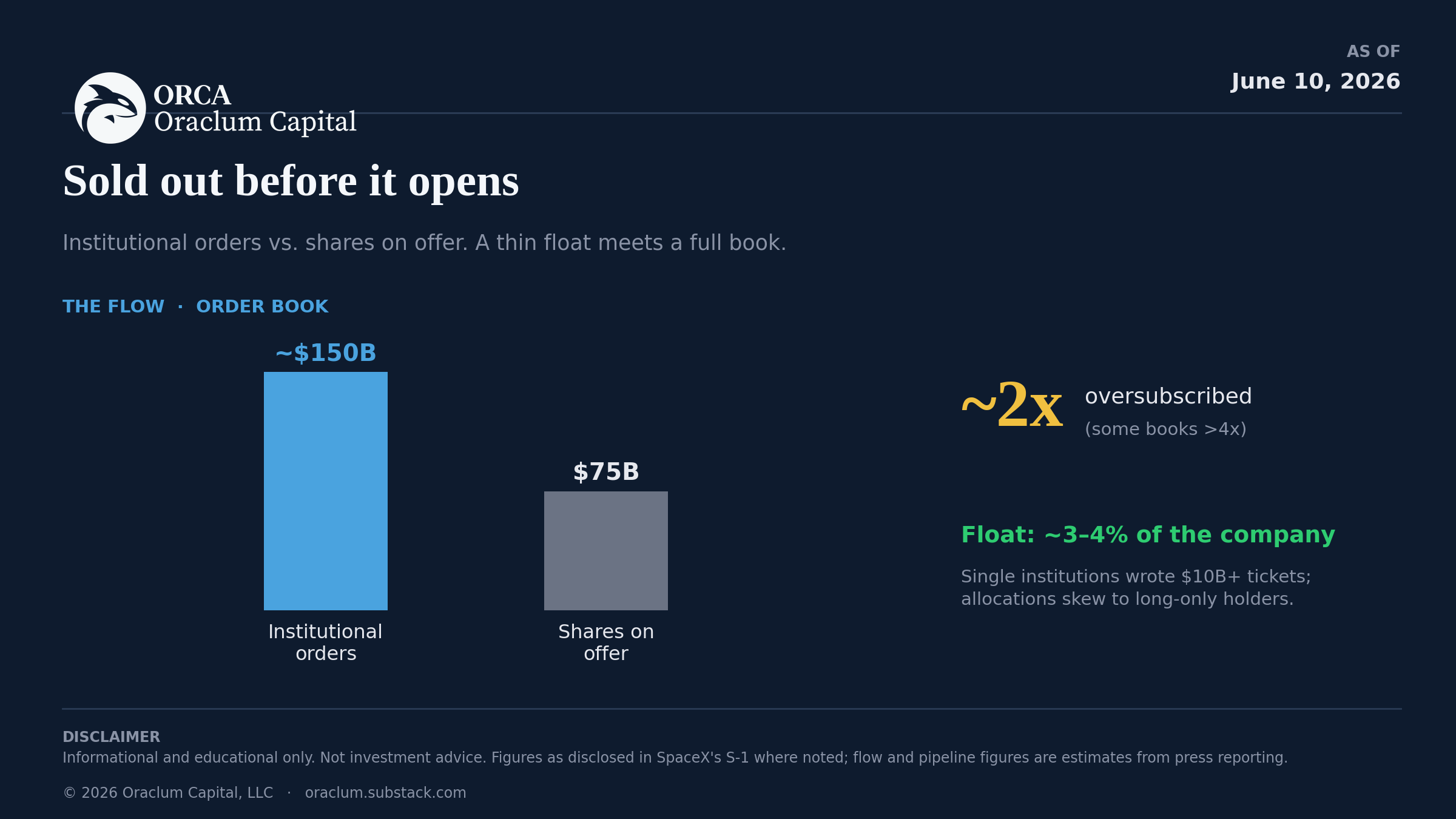

Fundamentals and flow point opposite ways, but on Friday the flow might win. Book is 2x oversubscribed ($150bn in orders), retail gets the $135 price alongside the whales, and the float is a 3–4% sliver. Overpriced and gapping higher are both true.

Trade or fade? I’m gonna make you to read the whole thing before answering that question :)

The biggest IPO ever is here: SpaceX (SPCX). On Friday (tomorrow) at 9:30 it opens for trading (allow the first few minutes for the market makers to adequately price it). Options will begin trading on Monday.

So, what’s it all about?

$1.8tn for an AI company or Space exploration or an Internet provider?

I went through the SpaceX S-1 filing for its IPO over the past week. There is A LOT to unpack there. Let’s start with the general idea. The pitch you’re being sold with this IPO is that SpaceX is an AI company that happens to own some rockets. The filing says so in the first few pages: “the largest actionable total addressable market in human history,” $28.5 trillion, of which $26.5 trillion is artificial intelligence. The roadshow leans on it, and the valuation heavily depends on it. So it’s not a space company, as many would (safely?) assume. It’s an AI company.

The income statement tells a different story. Strip out the vision and SpaceX is a satellite internet provider with one very expensive science project bolted to the side and a second one - xAI - that loses money roughly as fast as the first one makes it. That gap, between the company being sold and the company that exists, is the whole trade. On Friday you’ll find out what the market wants to pay for the difference.

So let me do what the roadshow won’t. Follow the cash, and separate the three businesses people keep mashing into one ticker. Then we’ll talk about whether the buying - institutional and retail - is strong enough to hold $135 regardless of any of it.

The $28.5 trillion number is wishful thinking, not a target

Start with the TAM, because it tells you who the deal is built for.

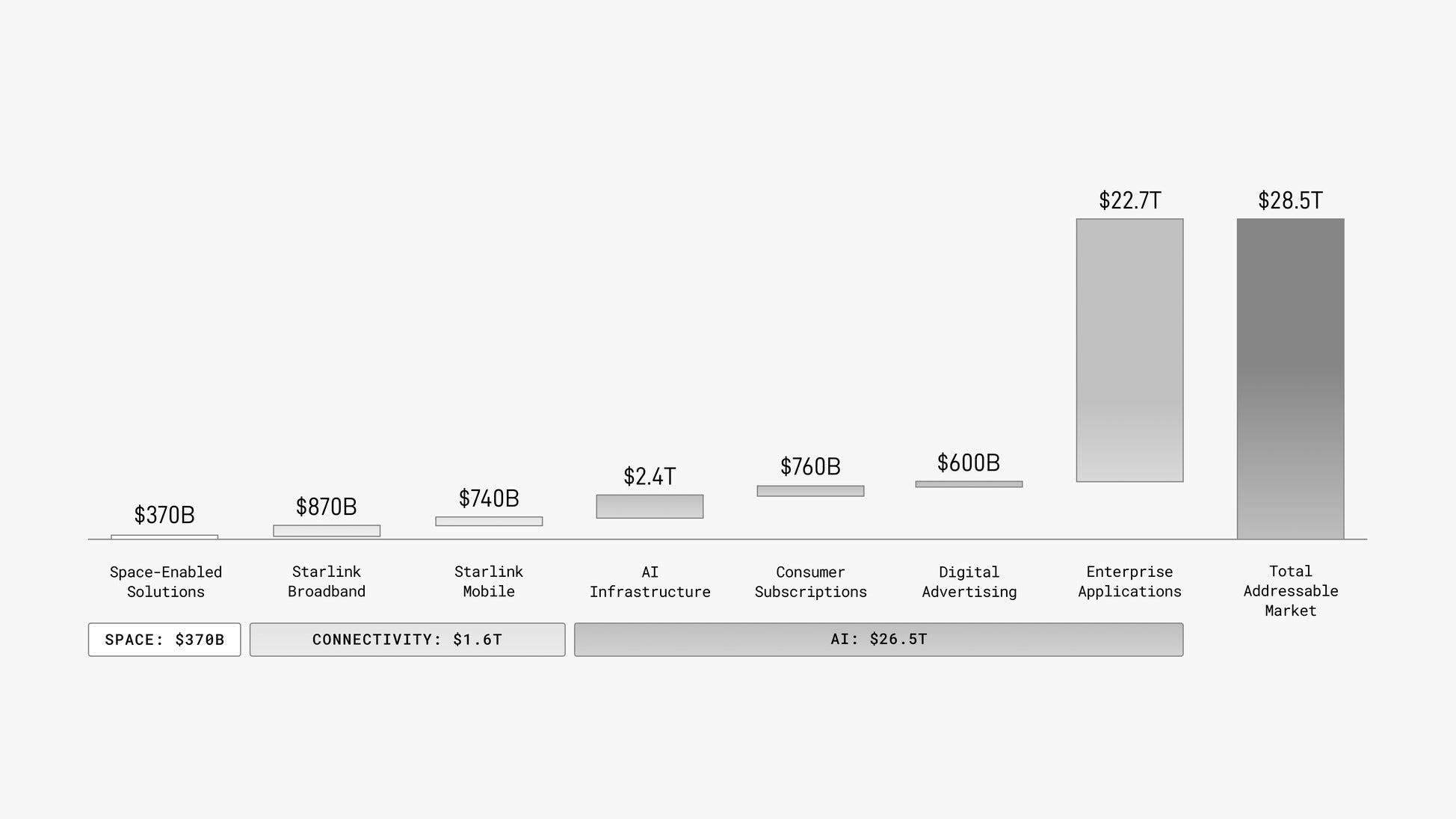

SpaceX puts its addressable market at $28.5 trillion and calls it the largest actionable opportunity in human history. For scale, that’s about a full year of US GDP. The breakdown, straight from the S-1:

Space: $370 billion. Launch, national security, NASA, the stuff SpaceX actually dominates.

Connectivity: $1.6 trillion. Starlink broadband ($870B) plus Starlink Mobile ($740B).

AI: $26.5 trillion. This is 93% of the whole number.

Now open the AI box, because that’s where the honesty runs out. The $26.5 trillion is: $2.4 trillion in AI infrastructure, $760 billion in consumer subscriptions, $600 billion in digital advertising, and $22.7 trillion in “enterprise applications.” That last bucket alone is bigger than the combined GDP of every country on Earth except the US and China. It is, functionally, “the future economy, assuming AI eats most of it, and assuming we get a cut.” The filing even notes the estimates exclude China and Russia - as if the constraint on a $22.7 trillion number is geographic access rather than its complete detachment from anything you can underwrite.

I want to be fair about what a TAM is. It’s a ceiling, not a forecast, and every S-1 inflates it. But there’s a difference between Uber claiming all of personal transportation and a rocket company claiming a double-digit-trillion slice of all enterprise software on Earth. The first is aggressive. The second is wishful thinking. The number isn’t there to be defended. It’s there to reframe the conversation away from a satellite ISP doing $19 billion in revenue and toward a civilization-scale AI platform, so that 94-times-sales feels like a discount instead of a dare.

That’s the tell. When the addressable market is 1,500 times current revenue, management is asking you to price the story, not the business.

Follow the cash, and the company gets a lot smaller

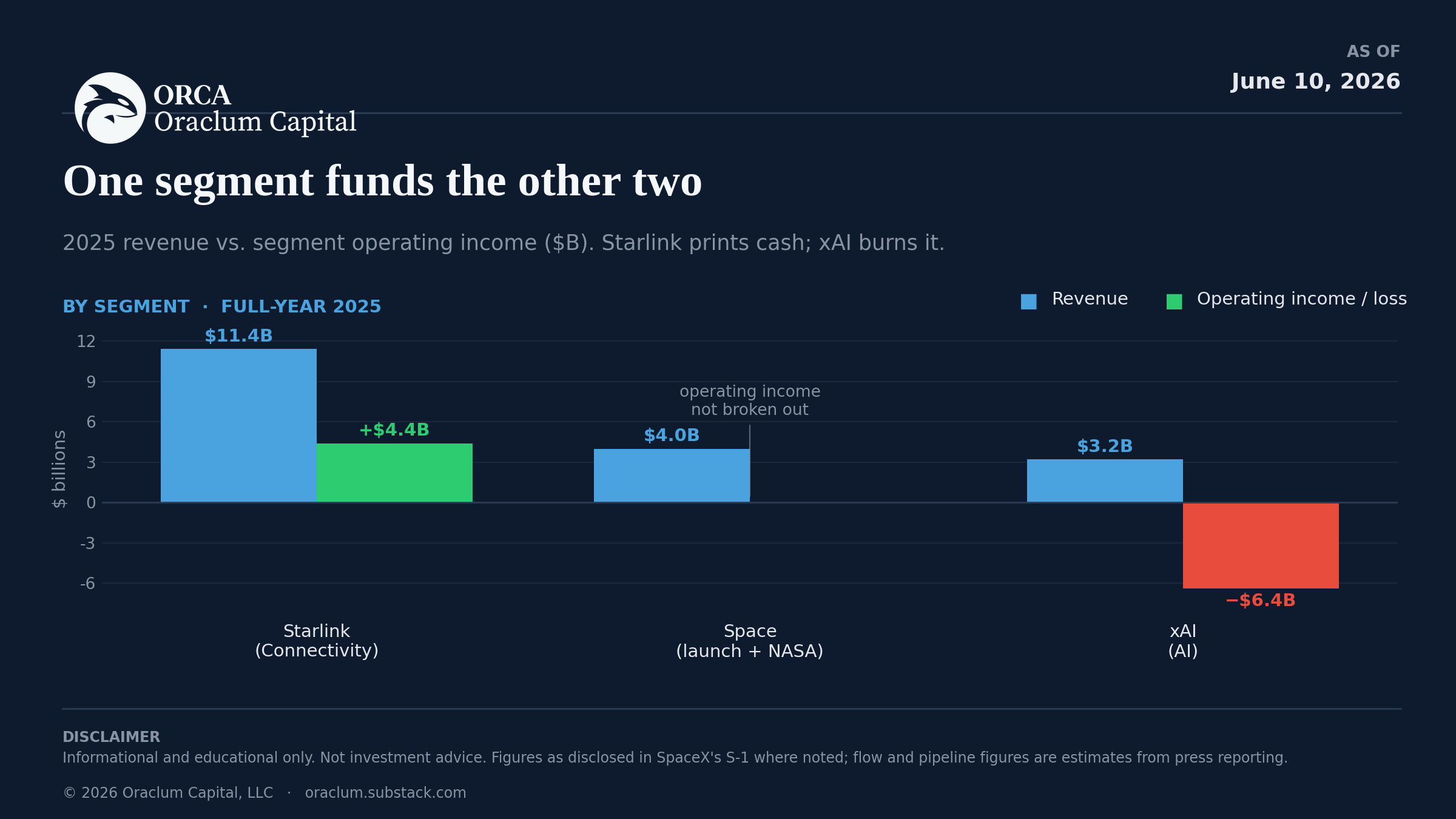

Here’s what SpaceX actually did in 2025: $18.7 billion in revenue, a $2.6 billion operating loss, and $6.6 billion in adjusted EBITDA - the non-GAAP figure they’d very much like you to anchor on. Three segments which could not be more different in quality:

Connectivity (Starlink) - $11.4 billion, 61% of revenue. Up nearly 50% year over year, with $4.4 billion in segment operating income. By Q1 2026 it was running at $3.26 billion a quarter with a 36% operating margin and 10.3 million subscribers across 164 countries. This is the company. It’s the only segment that prints cash, it’s growing like a software business, and it has a structural moat that a competitor cannot copy without first building a reusable rocket and launching 9,600 satellites. Starlink is genuinely one of the best infrastructure businesses created this century. Kudos to Musk on that one.

Space - about $4 billion, 21% of revenue. Launch, crew, national security. SpaceX put more than 80% of all mass to orbit globally every year since 2023. It has a 99%-plus Falcon success rate. It is, by a distance, the most capable launch provider that has ever existed. It’s also the smallest of the three segments by revenue, and Starship - the thing the entire future depends on - burned $3 billion in R&D last year and hasn’t delivered a payload to orbit yet. The crown jewel of the brand appears to be the least of the three.

AI (xAI) - $3.2 billion, 17% of revenue, and a $6.4 billion operating loss. SpaceX folded xAI in via an all-stock deal in February 2026. In 2025 the unit lost roughly twice its revenue. It’s on pace to burn about $10 billion in 2026. As a comparison, did you notice that Google is planning to spend $180-190bn on it’s own AI capex, and they had to raise cash for it by selling $85bn of its equity, plus a $10bn infusion from Berkshire - just to put things in perspective.

Basically, Starlink’s entire annual operating income doesn’t cover xAI’s annual loss. The most valuable, fastest-growing part of the story is also a furnace you’re being asked to feed.

Put the three together and the picture is almost comic in its imbalance. A world-class cash machine (Starlink) is funding a world-class capital sink (Starship) and a separate, larger cash sink (xAI) at the same time. The bull case is that all three are the same flywheel. The bear case is that you’ve stapled three companies together and slapped one $1.8 trillion price tag on the bundle because two of them have better stories than Starlink’s boring, profitable broadband.

What actually drives it: the AI trade, Starlink, or space?

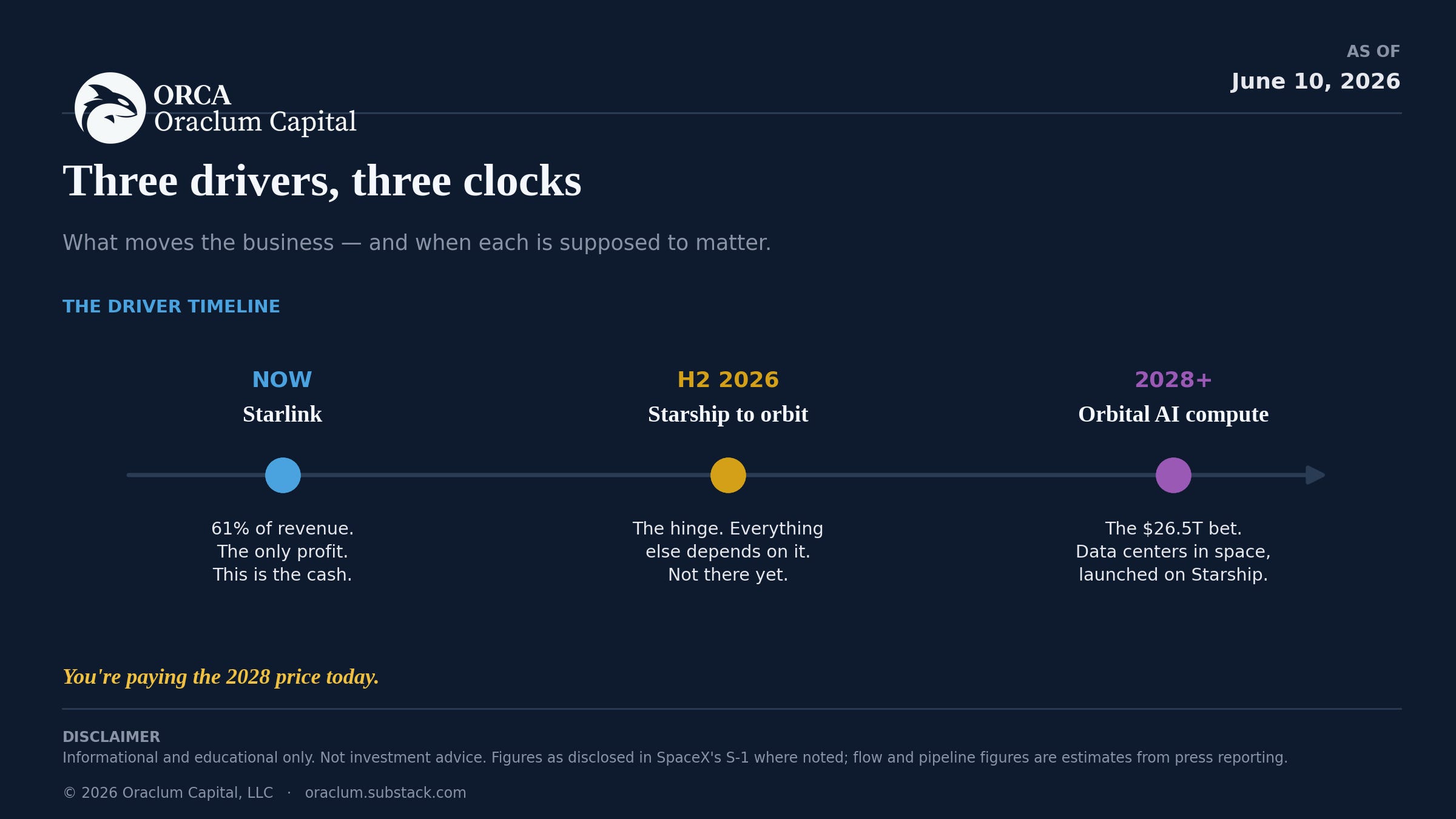

The three drivers operate on completely different clocks.

Today, it’s Starlink. Every dollar of profit, the whole subscriber-growth story, the only defensible margin in the building. If you’re buying SPCX on fundamentals you can touch, you are buying a satellite ISP and paying a launch-company premium and an AI-company premium on top. The honest valuation question is: what is a 50%-growth, 36%-margin connectivity business worth, and how much of the other $1.5 trillion-ish is faith?

The hinge is Starship. Almost nothing in the vision works without it. Next-gen Starlink satellites, satellite-to-phone service, the Mars architecture, and - critically - the orbital AI data centers all assume Starship is flying cheaply and often. It isn’t yet. Payload to orbit is promised for the second half of 2026. So Starship is the single variable that converts the cheap story (broadband) into the expensive one (everything else). Watch the flight cadence more than any earnings line. That’s the real fundamental catalyst, and it’s binary in a way revenue never is.

The AI bet is a lottery ticket priced like a sure thing. SpaceX’s actual AI thesis isn’t just owning xAI - it’s space-based compute. The filing argues the Sun holds 99.8% of the solar system’s energy and that orbital solar is the only scalable answer to AI’s power problem, with the first orbital AI-compute satellites slated for “as early as 2028.” Read that sentence again. The bridge from a furnace losing $10 billion a year to a $26.5 trillion market runs through data centers in orbit launched on a rocket that hasn’t reached orbit with a payload yet. It might be visionary. It might be the most expensive distraction in corporate history. What it is not is something you can put in a 2026 DCF.

And there’s a circularity worth flagging. In May 2026, xAI signed cloud-services agreements with Anthropic worth about $1.25 billion a month through 2029 - roughly $45 billion - to fill its Colossus data centers. That’s a real, large, third-party contract, and it’s the closest thing the AI segment has to underwriting. It’s also a reminder that today’s AI revenue is infrastructure rental, not the $22.7 trillion enterprise-software dream. The money xAI makes right now comes from renting out GPUs, the same commodity business everyone else in AI is also racing into, at a loss.

So the answer to “what drives it”: Starlink drives the cash, Starship drives the option value, and AI drives the multiple. You’re being charged for all three. Only one of them is real yet.

The one disinterested number in the room

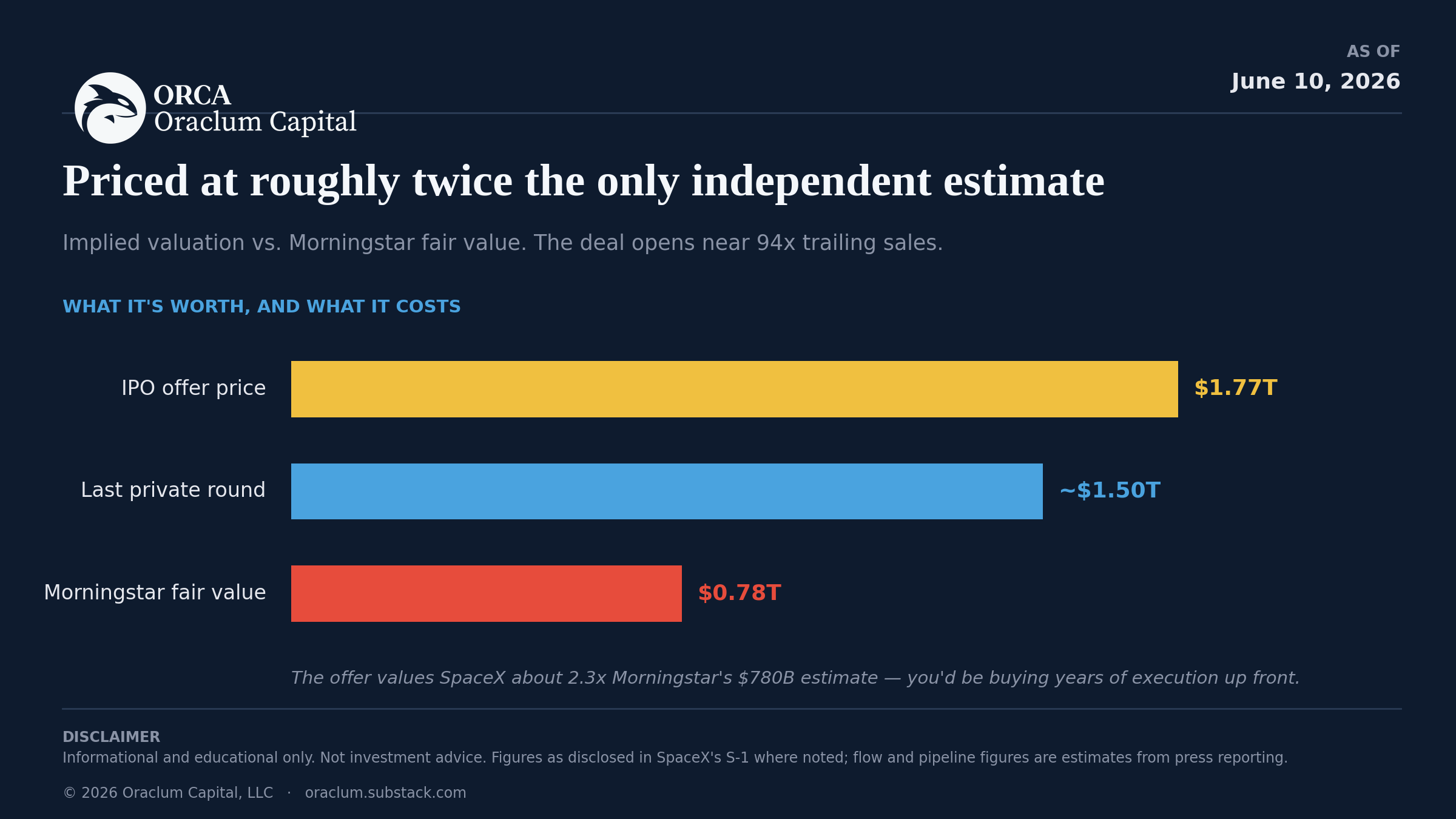

Everybody quoted in this deal gets paid if it goes well. The banks, the company, the early holders, the financial media chasing the biggest IPO ever. There’s exactly one number from someone with no skin in the placement: Morningstar’s fair value of $780 billion.

That’s about 55% below the $1.75 trillion IPO target, and still well under SpaceX’s last private mark near $1.5 trillion. Morningstar’s reasoning is the same one the segment math points to: Starlink is excellent and worth a lot, Space is solid, and xAI is a “material threat of value destruction” with an “indeterminate” moat. At $135 the deal prices at roughly 94 times sales. As one analyst put it, you’re being asked to buy 2030 at the 2026 offer price.

You don’t have to agree with Morningstar’s number. You do have to explain why you’re paying double it. And the answer most buyers will give isn’t about discounted cash flows. It’s about flow.

The flow: who’s actually buying, and why it might not matter that it’s overpriced

A stock doesn’t need to be cheap to go up on day one. It needs more buyers than sellers into a tiny float. On both counts, this deal is built to pop.

Institutions are in, and it’s not just Jamie Dimon doing the convincing. Quick correction to a storyline going around: this is Goldman Sachs’ book to run, with Morgan Stanley and Bank of America alongside and JPMorgan one of five bulge-bracket names on the cover, not the lead. So the question isn’t really whether Jamie Dimon can rally Wall Street behind Musk - the two have their own history - it’s whether a 21-bank syndicate can place $75 billion into a market that’s been hoarding cash for exactly this kind of deal. The early read says yes, easily. By this week the book was reported more than two times oversubscribed, with total orders around $150 billion against the $75 billion on offer, and multiple single institutions writing tickets of $10 billion or more. The banks signaled allocations would skew to long-only managers - the sticky, low-turnover money you want holding the float steady, not flipping it. Institutional books close at 4pm New York today. Pricing is tomorrow.

That oversubscription is the real institutional signal, and it’s worth being precise about what it means. It does not mean the institutions think SpaceX is worth $1.8 trillion. It means they think it’ll trade above $135 in week one and they want allocation before it does. Those are very different beliefs. A long-only manager can rationally buy a stock he thinks is 30% overvalued if he’s confident the next buyer pays more - and into a 3–4% float with this much retail behind it, that confidence is cheap to hold.

Retail isn’t waiting on the open this time. The structural twist of this deal is that SpaceX and the banks are letting retail buy at the $135 IPO price, simultaneously with institutions, through Schwab, Fidelity, Robinhood, SoFi and E*TRADE. That almost never happens. Normally retail’s job is to buy the pop from institutions who got the IPO price; here they’re being handed the same entry. There’s even a dedicated retail roadshow event. Demand is expected to swamp the allocation, so most retail orders get partially filled or not at all - which, if you’ve ever watched a hyped IPO, only makes people want it more.

So will retail flock? Yes, most certainly. It’s the most famous founder in the world (shorting Musk’s companies was historically a bad trade), the biggest IPO in history, the first real chance to own the SpaceX/Starlink/xAI story directly, and a price that feels “official” because it’s fixed. Retail isn’t underwriting on the income statement and cash flow. They’re buying the man, the mission, and the fear of missing (FOMO) the one they’ll tell stories about. Musk’s base buys conviction, not multiples (just have a look at TESLA multiples right now), and a fixed $135 price - which signals control rather than the usual price-discovery range - is practically designed to read as “the company is telling you what it’s worth” rather than “the banks couldn’t find the clearing price.”

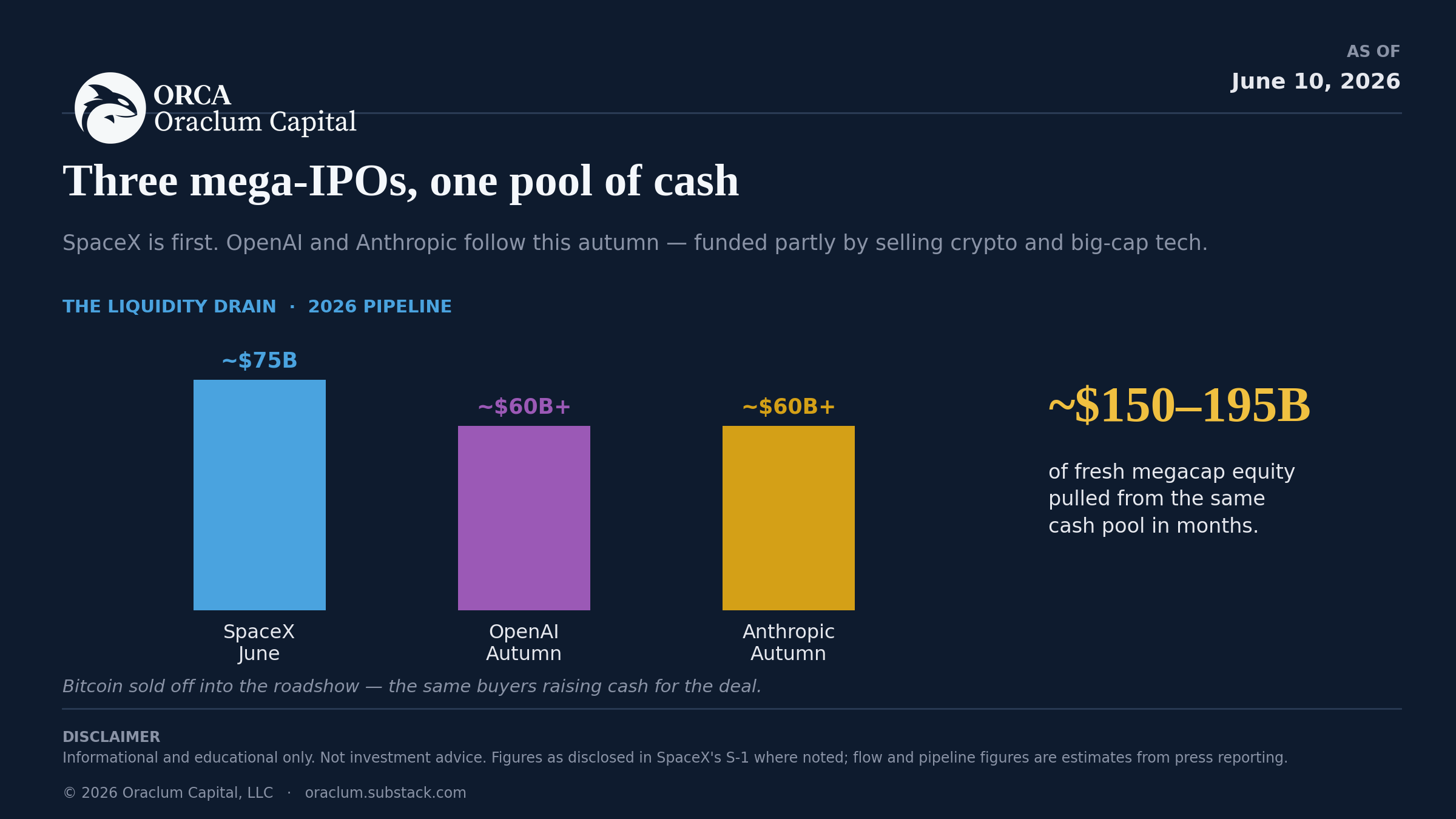

Where does $75 billion come from? Probably your other holdings.

Here’s the part the bulls skip. A $75 billion deal doesn’t conjure $75 billion of new money - it pulls it from somewhere, and the leading suspect is the rest of the risk-on book. The cleanest tell is Bitcoin, which sold off hard into the roadshow. The theory making the rounds, floated by Bitwise among others, is that the SpaceX crowd and the crypto crowd are largely the same crowd, dumping BTC to free up cash for an allocation they actually want. Same mechanic in equities: the estimates going around have retail and passive investors selling something like $50 billion of other stocks to fund SPCX, which is why you’re seeing odd dislocations this week in names that have nothing to do with rockets. When a buyer needs cash for the biggest IPO in history and the float is a sliver, he sells what he can, not what he wants to. The deal doesn’t add to the risk pool. It drains it and re-pots the money into one stock.

And SpaceX is only the first of three. Anthropic filed on June 1 at roughly $965 billion. OpenAI filed confidentially a week later, valued somewhere between $850 billion and $1 trillion, eyeing an autumn listing. Each wants to raise $60 billion or more. Stack them and the market is being asked to swallow on the order of $150–195 billion of fresh megacap equity in a matter of months - a several-fold jump in IPO supply, all of it fishing in the same pond of cash. That money comes out of the existing Mag7 and whatever’s liquid in the speculative corner. So the SpaceX flow isn’t just a one-day squeeze in SPCX - it’s the opening move in a liquidity drain that reloads in the fall. If you hold crypto or big-cap tech, there’s a decent chance you help fund this IPO whether or not you ever place an order, and then help fund the next two. The thing to watch isn’t just whether SPCX pops. It’s what gets sold to pay for it.

Here’s the uncomfortable synthesis. The fundamentals say overpriced by roughly half. The flow says it gaps higher anyway. Both can be true, and on Friday they probably will be. A thin float plus a sold-out institutional book plus retail buying at the same price as the whales is the recipe for an open well above $135 - and none of it requires the valuation to make sense. It requires only that the marginal buyer believes there’s another buyer behind him. For a while, there most certainly will be.

However, don’t be fooled by the forced buying narrative.

The mechanical index bid here is real but small, and it’s Nasdaq, not the S&P 500. The S&P kept its 12-month seasoning rule at its June 4 review and SpaceX fails the profitability and float screens anyway, so S&P 500 inclusion is years away, not weeks. Nasdaq’s new fast-entry rule does let SPCX into the Nasdaq-100 after about 15 trading days - but the same rule caps a low-float name at three times its float-adjusted market cap, which knocks a $1.8 trillion headline down to a $225 billion effective weight. Enter SpaceX at a $225bn effective weight into a Nasdaq-100 whose aggregate runs north of $30 trillion, and you get an index weight around 0.7%. Passive money directly tracking the index - QQQ at $435 bn, QQQM at $72 bn, plus the smaller trackers - is on the order of $600 bn. Multiply it out: roughly $4 billion of mechanical buying, and that’s the high end. Phased in tranches, the day-one number is smaller. Therefore, the resulting passive buy is on the order of a few billion dollars against a $75 billion float. It’s real, and it’s roughly 5% of the deal, but it’s not what re-rates this stock, and anyone selling you “index inclusion forces institutions in” is selling the tail as the dog.

Trade or hold?

Depends on your view. If you don’t like the fundamentals, stay away for now. Don’t get sucked into something just over FOMO. Yes, the speculative element will be massive, but is that something that attracts you? If no, stay away. If yes, good luck!

But let’s say you reaaally like this company, and/or are a big fan of Musk. Fair enough, it probably worked for you in the past, it might work now as well. The price could skyrocket initially on Friday and then come crashing down soon afterwards (as initial post-IPO profit-taking takes place). If you wanna time it, don’t! You’ll miss it almost certainly. It can keep going up and keep pricing you out, or it can crash down and you’ll feel terrible for jumping in too early. So if you’re a “buy and hold” investor, don’t second guess your entry point. Best option is to buy outright with a small part of your portfolio (the one designed for risky trades in your barbell strategy) and forget about it. Close your nose at the price, basically.

And just think that it might deliver just like all the Mag7 stocks overtime. If that’s your risk preference and time horizon, doesn’t really make a difference when you get in.

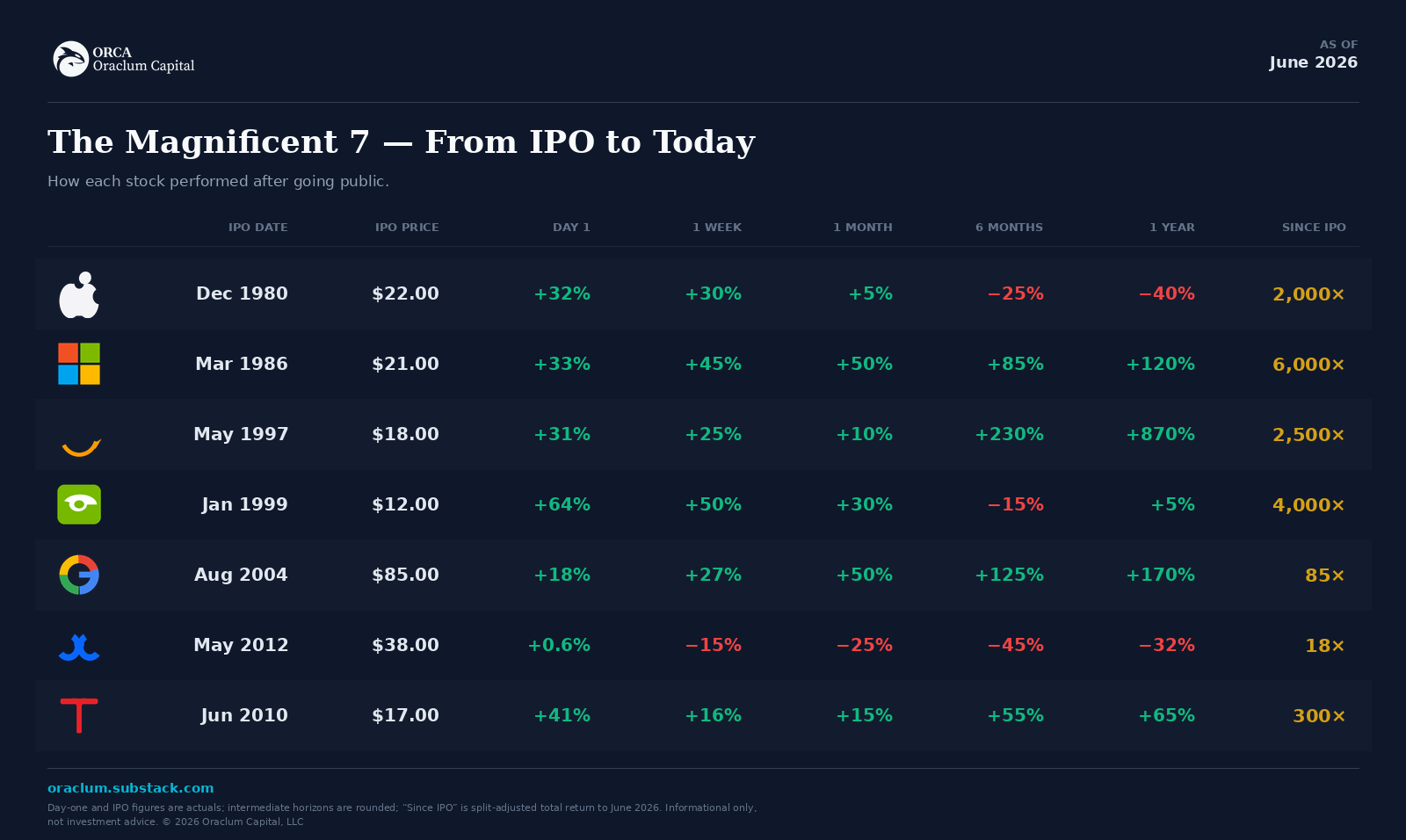

If this is the case, here is a brief overview of how the Mag7 stocks did in their IPOs:

As you can see the day-one pops were the norm except for Meta. The effect was typically +30-40% first-day jumps (AAPL, MSFT, AMZN, TSLA). Google’s was somewhat tamer at +18%, NVDA was over 60%, and Meta’s was the infamous flat open that became a year-long slide (down 45% within six months). Different times!

But basically, the first year was a poor guide to the next 40. Apple and Nvidia were down and flat a year after IPO; Meta was down a third - yet all are now multi-thousand-percent winners. Buying the IPO and holding was the trade; timing the first year was noise. The 1980s-90s names (Apple, Microsoft, Nvidia, Amazon) compounded into thousands of times from their IPO price. The 2004-2012 names (Google, Tesla, Meta) are “only” tens-to-hundreds of times - still extraordinary, just less runway.

Will the same happen to SpaceX, Anthropic and OpenAI?

Yeah, very likely. But if you wanna buy and hold, best view is to do it and forget about it. Disregard the noise that will happen on Friday and in the coming weeks.

And DO NOT expect this to be a multibager on first day or first few days. It might, of course. With the benefit of hindsight, all of these were. But the very last thing you wanna do here is to try and time it. Either stay away if you don’t believe in it, or buy and hold and do not speculate with it.

Thanks for reading! And thanks for subscribing to the newsletter.

Don’t forget to tell your friends.

Or as the YouTube generation says Like, Share, Subscribe:

DISCLAIMER: Neither the survey nor any of the contents of this website can act as investment advice of any kind. The results of the survey need not correspond to actual market preferences or trends, so they should be interpreted with caution. Oraclum Capital, LLC (Henceforth ORCA) is a management company responsible for running the ORCA BASON Fund, LP, and for organizing a survey competition each week, where it invites the subscribers to its newsletter (this website) to participate in an ongoing prediction competition. The information presented on this website and through the survey competition should under no circumstances be used to solicit any investment advice, nor is it allowed to be of commercial use to any of its readers. The survey and this website contain no information that a user may use as financial or investment advice. All rights reserved. Oraclum Capital LLC.