What will Q1 earnings tell us?

Paid subscriber analysis

Dear readers,

before we dive into today’s topic - on what we might find out from Q1 earnings and how this could impact the market going forward - we’d like to invite you to do a very quick, 2-3 minute survey for us.

It’s a total of 6 questions, none of them asking any personal info, designed to explore your investing approaches. Your responses will help us tailor our content to better suit your needs.

Thanks for that!

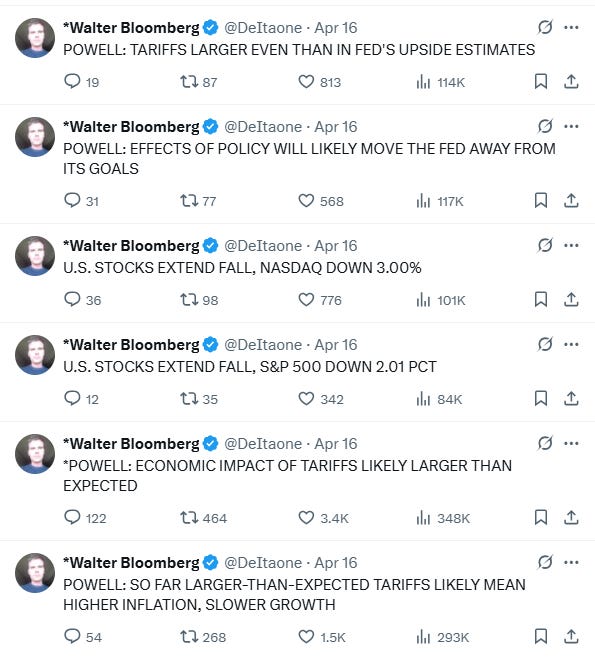

This week was shorter due to Good Friday (happy Easter btw!). But this doesn’t mean we didn’t get our usual jumpiness. On Wednesday Fed Chairman Jerome Powell crashed markets (-3% SPX, -4% NASDAQ) at a conference keynote speech, after expressing concern over how tariffs would affect inflation, and signaling the Fed won’t be cutting rates or supporting markets. After statements like these, no wonder the effect was an immediate sell-off:

And then the next day, Trump fired back:

In our outlook for 2025 we have talked about a possibility of a clash between Trump and the Fed and that this might be one of the main battles of 2025. Well, tariffs took the headlines thus far, but with Powell standing firm there is an increasing possibility of the Trump administration already finding a replacement to serve as a shadow Fed Chairman before Powell’s term ends (May 2026). If that does happen, market expectations will start anchoring around the shadow Chairman very quickly. Let’s hope it doesn’t come to this, as this could bring even more turbulence to markets, and a certain second-leg major sell-off. I read a comment on X saying (paraphrasing): “if Trump fires Powell, the finance community will make Jan 6th look like a picnic.” Yeah. Very likely.

On Thursday again sideways; SPX went from negative to over 1% at one point only to crash back down before the end of the day. Why the intraday bounce? Some of it was driven by Trump announcing they are very close to their first trade deal with - surprise, surprise - Japan.

Remember what we said last week in the paid section? We presented an overview why Japan would be the ideal first trade deal for the Trump administration:

…Trump will declare many victories in the weeks to come, but his first target will most likely be Japan.

Japan is one of the most important American trading partners, and a country that depends a lot on US trade. America is Japan’s no 1 export market, capturing 21% of all its exports. The second is China, with 17%. Japan imports 22% from China, and 12% from the US. For them US tariffs are clearly a big hit, and given that the two countries are important strategic partners (and both see China as a big threat), it is of interest to both that the first trade deal is struck there. This then sends a signal to others on how to position. I would not be surprised to see this deal happen first.

The tariff war with China is still in escalation mode and there is no progress yet with the EU, but as we mentioned, the Trump administration’s primary focus is Asia. Expect more deals to come from those countries, circled around China (S. Korea, Taiwan, Vietnam, India, etc.). The EU will just have to wait.

Q1 Earnings: what to expect?

Our primary focus today is on Q1 earnings.

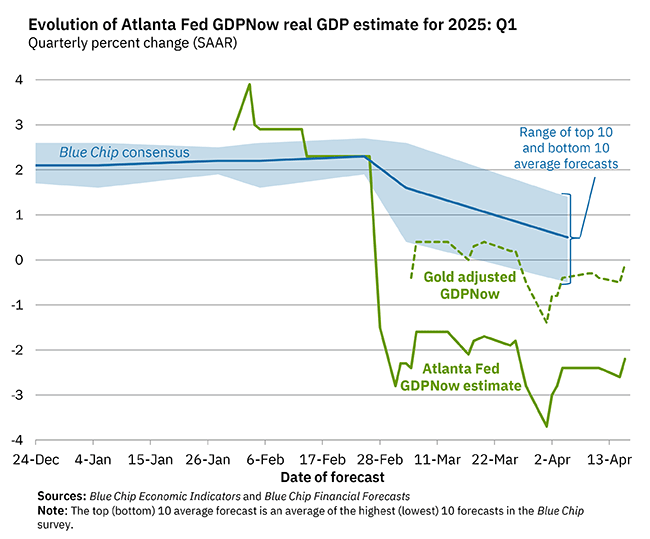

First, a macro overview. As you may be aware by now, the Fed GDPNow estimate for US Q1 GDP growth is at -2.2% (down from 3% just two months prior). This is the immediate impact of tariffs on US GDP, led my massive frontrunning of imports (we wrote about that here). But even when adjusted for the imbalance between imports and exports of gold (see here), the estimate for Q1 is -0.1%. A clear slowdown, on the verge of recession, especially if tariffs remain in place in Q2 and beyond.

This is important as it tells us what we can expect from earnings. Throughout 2023 and 2024 when earnings seasons came, there was little fear about earnings being worse than expected primarily because quarterly GDP grew at 2-3%. So if consumption is up, if private sector investments are up, and if government spending is up, there is little reason to expect poor company performance.

Currently the situation is reversed. We are back in the 2022 regime of declining growth and, consequentially, negative earnings expectations. Back then the growth shock came in the form of high interest rate expectations. Just a reminder, interest rates only began to rise in March 2022, and by the end of Q2 were at 2%, while GDP growth in those two quarters was negative, triggering a “technical recession”.

Company earnings very much reacted to this, albeit with a certain lag of a few months. Specifically, as Q1 GDP was going down, earnings per share (EPS) expectations started to adjust and went down in over the next three quarters, reaching a bottom in Q1 2023 - just as the market was starting its AI trade cycle.

Can we expect the same this time?