The final FOMC of 2024: what to expect?

Two weeks left to go in our competition!

The Q4 competition has two more weeks left to go - click here to join the action. Note: we will have the Christmas week active, as market is open on Thu and Fri. The survey will be open until Christmas Day, Wed, 25th, 8am ET, as usual.

This week is FOMC week, just in time to deliver an update to its summary of economic projections (SEP), thus presenting its own projections of the economy and interest rates in 2025. In terms of cuts, a 25bps is fully priced in. But all eyes are on SEP, and where the Fed sees interest rates for next year. Do we get a soft landing? Or does the bond market succeed in frontrunning the Fed?

Last Saturday, we presented our bear 🐻 view for 2025 to our paid subscribers—see here if you missed it. With both the bull 🐂 and bear 🐻 perspectives now covered, this Saturday we’ll wrap it all up with our 🦈 view, offering a balanced take on what lies ahead. Don’t miss it!

Paid subscribers also get a quick recap of the Fed decision and what it means for markets (both bonds and equities) on Wednesday soon after the press conference.

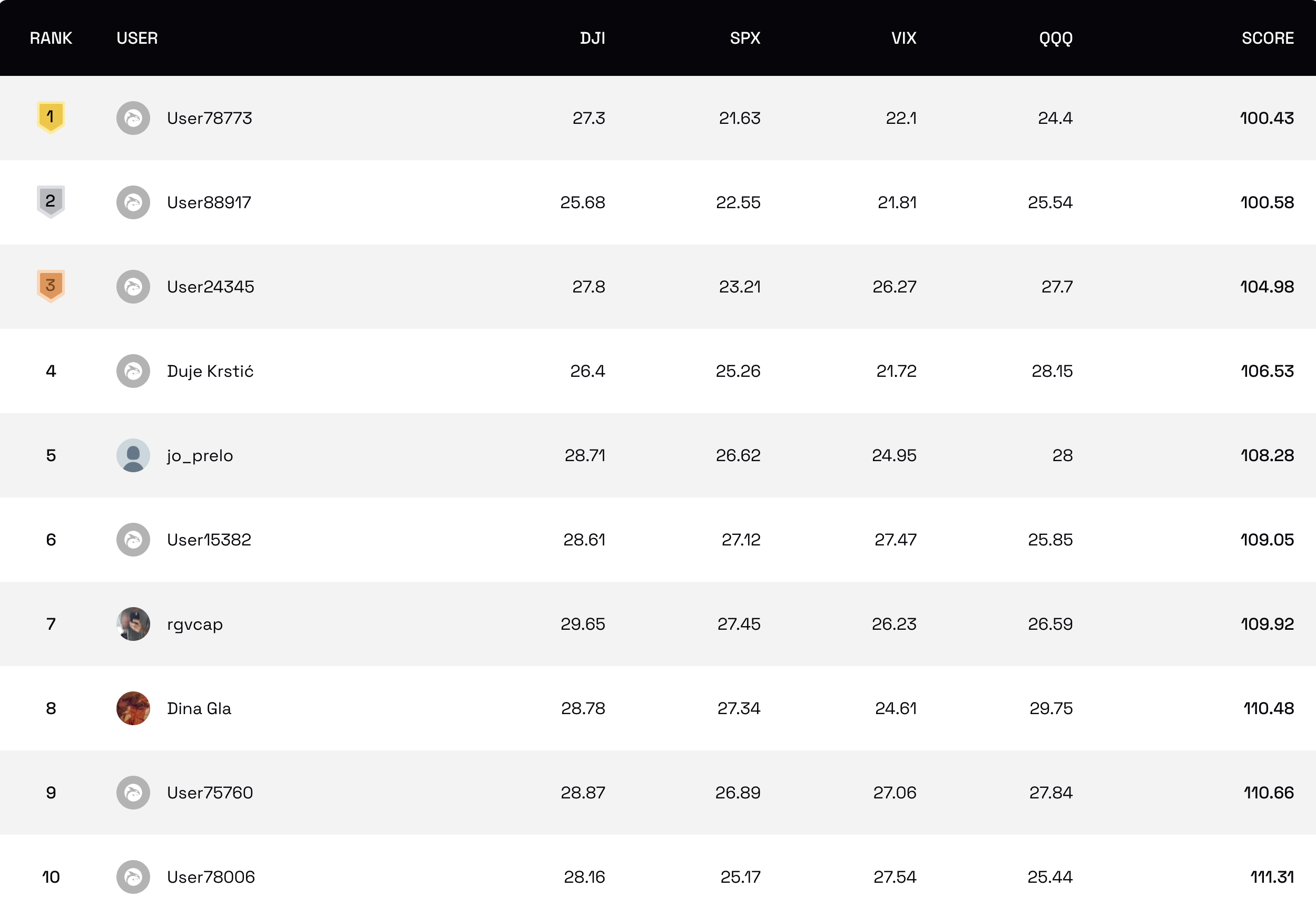

The competition

With the Fed’s final meeting of the year, this week is a great opportunity for your predictions to close the year on a high. The race for first place is again super tight!

NOTE: two more weeks are left, and we will have the Christmas week active, as market is open on Thu and Fri. The survey will be open until Christmas Day, Wed, 25th, 8am ET, as usual, so you will be able to make your predictions. We will place our positions the following day.

The survey will be closed in the first week of the new year, and will reopen on the 7th of January.

Keep your strategies sharp and your eyes on the top!

NOTE: For all those new to the whole thing, read more about it here or watch a video of Scott and myself guiding you through the survey, showing you all its features, and briefly explaining how the competition works.

Last week’s performance

CPI rose 0.3% from October, bringing the annual rate to 2.7%, with increases driven by shelter and food costs. Meanwhile, the PPI increased 0.4% for the month and 3% year-over-year, highlighting continued pricing pressures at the wholesale level.

As a result market action was quite jumpy last week. The CPI reaction was actually very positive, but over the next two days markets kept going down, erasing all of Wed gains, and even the brief Friday bump at the open. These are environments where we rarely make money, so last week we lost 1.4%. Still 30% up year-to-date (gross), but more on this in our final newsletter of the year in two weeks.

Anticipating FOMC

This week, the focus remains on the Federal Reserve as it concludes its final meeting of the year on Wednesday. There is a 98% chance the Fed cuts 25bps, so anything other than that would be a huge surprise: a pause would be a massive surprise to the downside and markets will sell-off hard, whereas a 50bps cut (zero chance of that) would be a massive surprise to the upside.

Any surprise, however, is highly unlikely. The rate cut will be 25bps. But everyone’s eyes will be on the summary of economic projections (SEP), where the Fed will present their outlook for interest rates, inflation, growth, and unemployment in the coming year.

This is what the market expects:

After this cut we get a pause in Jan, and then only two more cuts next year. The expectations are pinned at 3.75% to end the year. That’s a bit disappointing given how we entered 2024, expecting a much quicker return to 2-3% in the coming years.

With this in mind, the key number you should be looking at is the Federal funds rate projection. This was the number from the last SEP, in September, when the cutting cycle began and we got a 50bps cut:

For tomorrow, watch if the 3.4 number stays or gets adjusted to 3.6 or 3.7, where the market is currently pricing it, or worse at 3.9.

If it stays at 3.4 (and the long run stays at 2.9), the cut is announced, and Powell’s presser is at its usual dovish standard (the economy is doing well, inflation is going to target, still data dependent, rate cuts to continue at a slower pace, etc.) => expect a rally in equities.

If they raise rates to 3.6 (or worse) and the long run to 3.1, with a more hawkish Powell presser (inflation battle still not over, rate cuts much slower ahead) => expect a sell-off in equities.

Anything even more hawkish is an aggressive sell. Anything more dovish, an aggressive buy.

Personally, I do not expect the Fed to surprise markets this close to year-end. They are likely to stay the same course, despite the signals coming from the bond market, which is basically frontrunning the Fed. In other words, kick the can down the road a bit more, and wait until the catalyst for an equity sell-off comes from the bond market, not from them. This is the baseline expectation, so any surprise is obviously subject to a change in strategy. We will revisit on Wednesday.

Good luck in the competition!

…join the $20,000 competition!

Join our survey competition to get an opportunity to participate in our quarterly ($5000) and annual (3% of our profits) prize distributions:

DISCLAIMER: Neither the survey nor any of the contents of this website can act as investment advice of any kind. The results of the survey need not correspond to actual market preferences or trends, so they should be interpreted with caution. Oraclum Capital, LLC (Henceforth ORCA) is a management company responsible for running the ORCA BASON Fund, LP, and for organizing a survey competition each week, where it invites the subscribers to its newsletter (this website) to participate in an ongoing prediction competition. The information presented on this website and through the survey competition should under no circumstances be used to solicit any investment advice, nor is it allowed to be of commercial use to any of its readers. The survey and this website contain no information that a user may use as financial or investment advice. All rights reserved. Oraclum Capital LLC.

And, as always, don’t forget to subscribe to the newsletter.