When Second Leg?

Paid subscriber analysis

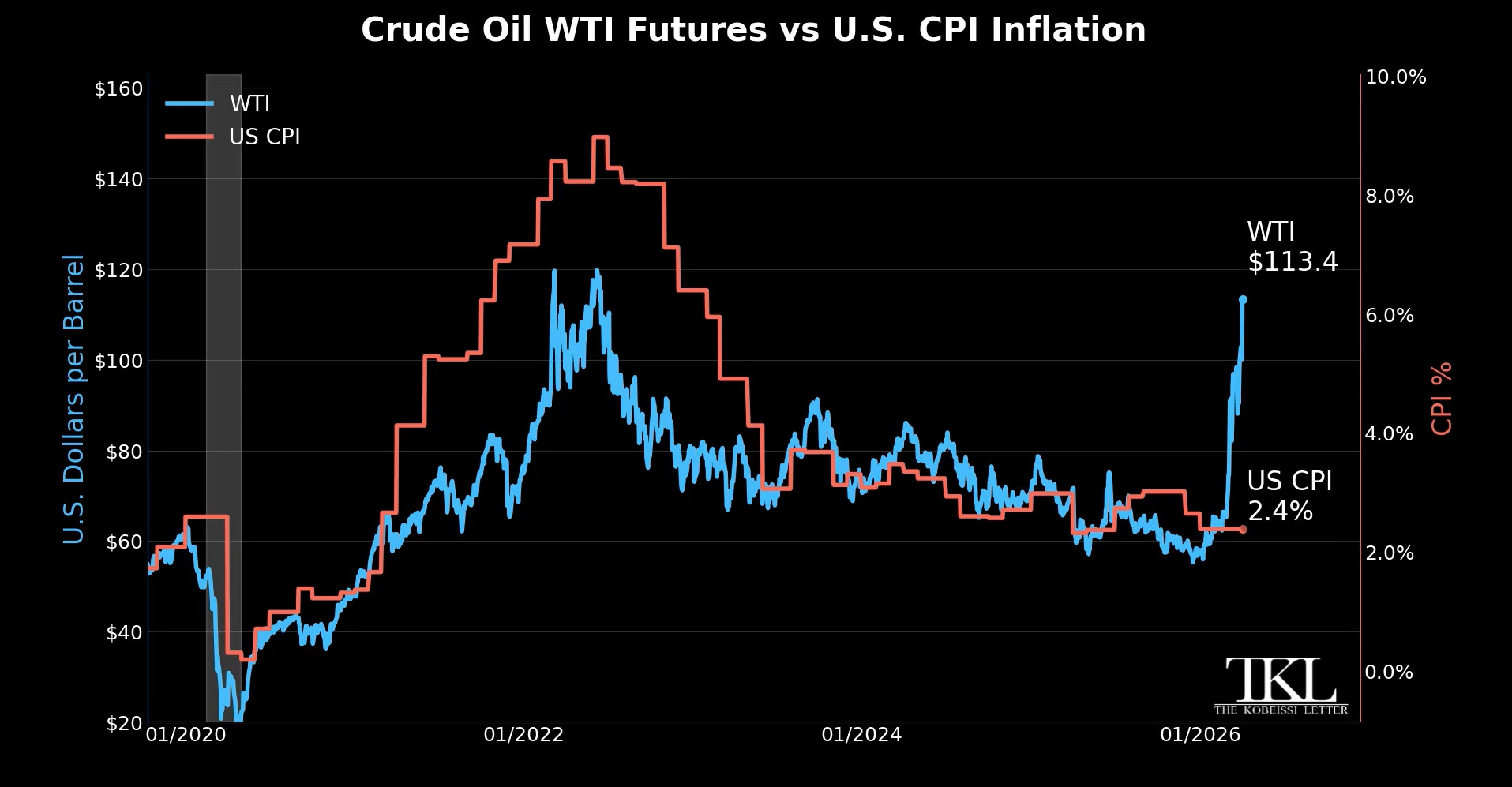

Last week ended with a very interesting decoupling of correlation between oil and equities. Oil jumped 12% on Thursday, last day of trading, following Trump’s press conference late night Wednesday where he didn’t show signs of backing out as was expected - quite the opposite, he talked about more bombings and more escalation. Oil prices shot up and ended the next day up 12%, finishing over $112 a barrel, and up over 90% in 2026 thus far.

Over the past 4 weeks this type of move sent shivers down the market and in each case resulted in a VIX spike and market sell-off. The correlation was very high, and you can clearly see vol gradually increasing with oil prices, even before the start of the war, just about as war fears were setting in.

But oddly enough, this Thursday we got a decoupling of this correlation. Oil was up 12%, VIX finished below 24 after close, and S&P and the NASDAQ were both flat for the day (after opening up -1.5%, they climbed back up intraday, most likely on the news that Iran and Oman are working on a Hormuz protocol). Even the bond markets took a breather, as the 10Y climbed down from 4.46% to 4.3%.

This could be a sign that we are past peak market panic over the Iran war. Meaning that the March >30 spikes in the VIX were likely the top in volatility for now. Which would consequentially mean the bottom for markets.

But let’s not get hasty. This is far from over.

Elevated oil prices will without doubt increase inflationary pressures, impacting consumers both directly (higher gas prices at the petrol station) and indirectly (e.g. businesses transportation costs go up which trickle down across the board).

The estimate from the Kobeissi Letter is that another 2 months of oil being above $100, we would see a rise of US CPI inflation to 3.3% (so almost 100 basis points from where it currently is).

And you know what that means: central banks will have to abandon rate cuts and either hold rates where they are (which is not priced in fully yet), or much worse - have to hike rates (not priced in at all).

This, in turn, brings us to the dreaded scenario of the Second Leg of the bear market.

The Second Leg is a typical bear market phenomenon. Think back to 2022. Usually there is some piece of change in narrative or change in macro conditions (back then it was the Fed signalling they will start to hike interest rates to combat inflation - deja vu anyone?) which triggers the first round of selling. In 2022 this lasted until mid March (until the FOMC meeting where the first hike happened). Then you get a series of violent bear market rallies - the typical short squeezes (closing shorts to take profits) that reinforce some automatic buying. This can last a few weeks and markets recover quite a bit of lost ground, but just as you think it’s all over (some higher highs and lower lows), we get an even more powerful second leg of the sell-off. Last time it lasted from early April to mid June and it took out 20% of the market. Then we got another rally into the summer and the final flush into September/October.

Will we get the same thing now? Every day with oil trading above $100 the probability of this scenario goes up.

Even if the war is resolved in the next 2-3 weeks, and if we are past peak market panic over the war, the oil shock is here to stay. And it will trigger a spike in inflation. The only question is: will central banks see this as another transitory shock or will it be more durable?

The JPM Collar Mar 31st rally

Last time, in the paid section, we covered this topic extensively. I warned you that end of quarter flows around the JPM collar do typically drive huge positive flows into the last few hours of trading.

The roll of the position on March 31st will be a high-liquidity event. JPM typically pairs the new collar entry with a deep-in-the-money (ITM) 0DTE call to balance the delta exposure during the transition. This maneuver can create an upward price pressure in the final two hours of trading, often resulting in a “rebound” on the last day of the quarter as dealers rebalance their books.

This typically starts to happen around 2pm EST … Note the March 31st, the move was +1.34% in the last two hours of trading, through to peak. That’s powerful. In Q2 the move was +0.57%, in Q3 the move was +0.69%.

This week, the move after 2pm was also around 0.7%, a great 0DTE trade. But this time the whole move started even earlier, at around 12:30, and delivered a cumulative 1.5% effect. No wonder we got a powerful bear market rally this week.

But will this rally persist?